The winter of 2019-2020 so far has been particularly challenging for natural gas producers attempting to transform themselves from growth engines to generating positive free cash flow. But all hope should not be lost, if history has taught us anything, falling natural gas prices lead to lower investment and generally a healthy rebound in the natural gas price in the year to come. Today’s energy market commentary will look at how prices have responded in the past to slowing upstream investment and how production should respond in 2020.

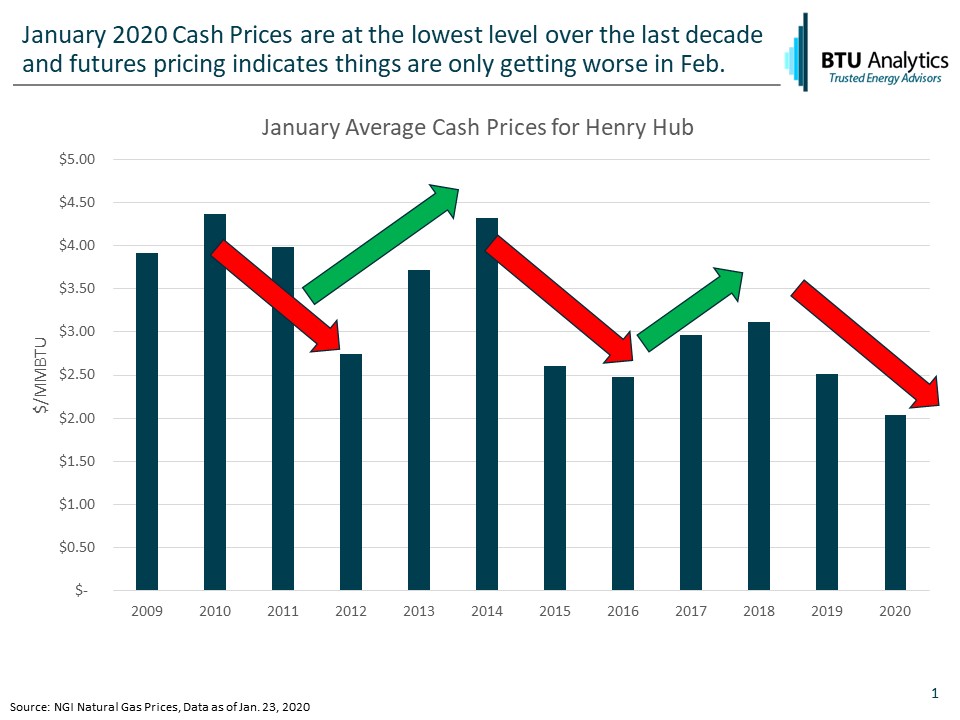

Cash prices in January have averaged a measly $2.04/MMbtu and NYMEX futures for Henry Hub are currently trading below $2.00 through April before beginning to recover to a staggering $2.60 in January 2021. The chart below highlights average January Henry Hub natural gas price since 2009.

The natural gas market over the last 10 years has generally been on a cycle of boom and bust driven by new record demand, followed shortly by new record levels of production that lead to busts in pricing. In 2012, that drove January Henry Hub pricing to $2.75, but the Polar Vortex in 2014 sent prices “skyrocketing” back to $4.32. At the same time, producers were rapidly growing in Appalachia and associated gas production was growing at a healthy clip driven by $100 oil. The winter of 2015 failed to deliver, and new production records cratered Henry Hub to an average of $2.54 for all of 2015 and 2016. With low oil prices crimping liquids rich investments, dry gas production unprofitable, and some help from old man winter, prices climbed back to $3.32 and $3.71 in 2017 and 2018 before starting the long downward slide to new lows for natural gas pricing in January.

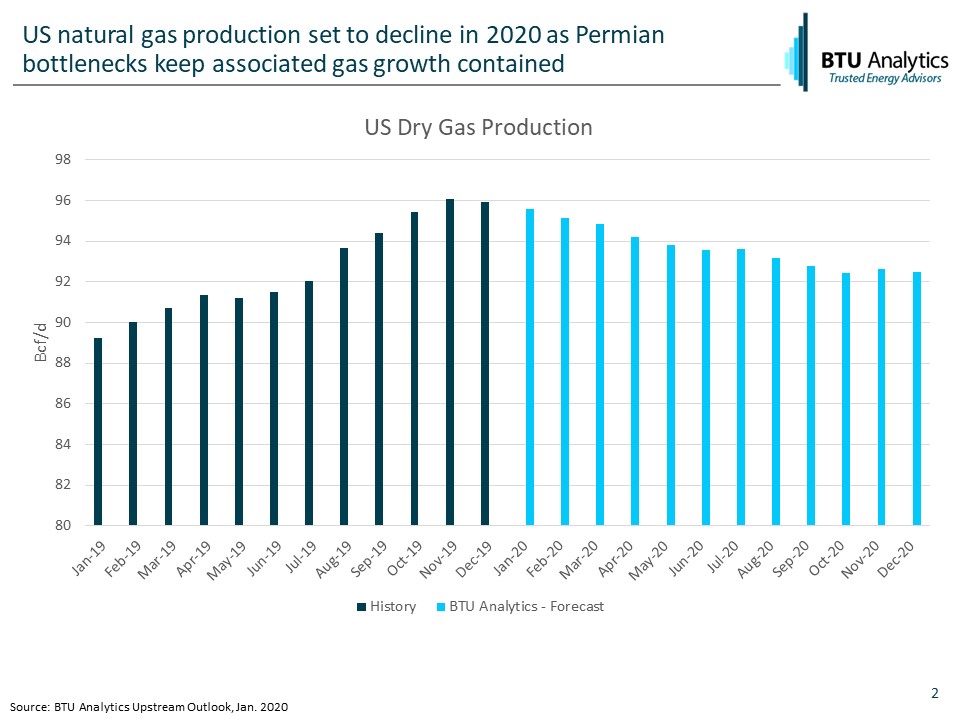

While storage levels will continue to remain above the 5-year average for most of 2020, natural gas production should not only fail to set new monthly records but enter into decline. The chart below is from BTU Analytics’ January Upstream Outlook.

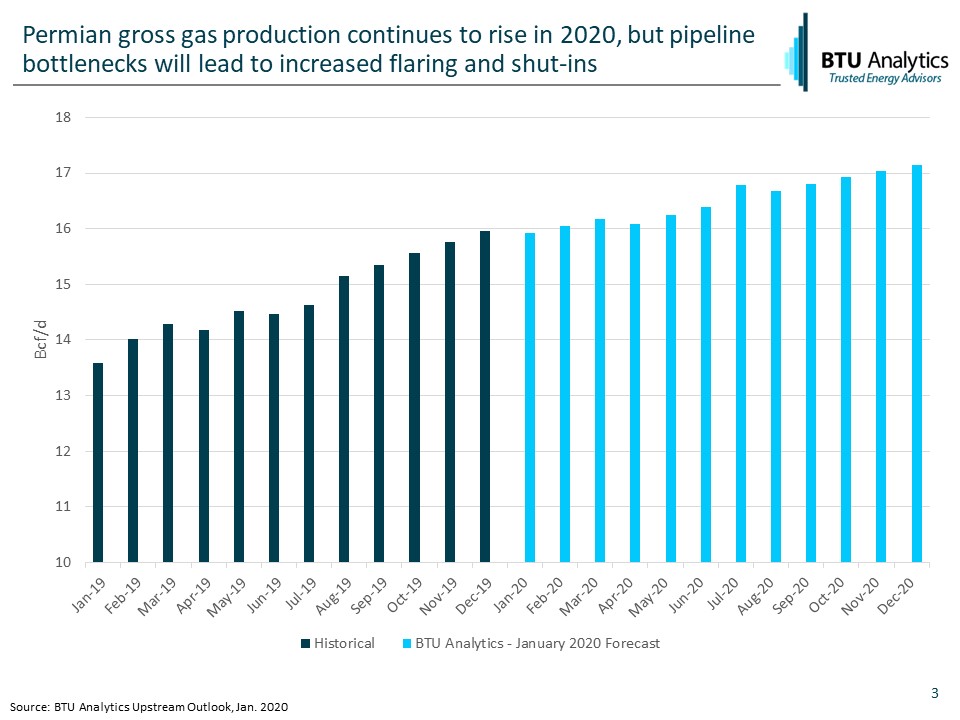

Without an uptick in drilling activity, natural gas production is poised to decline. While total dry production is in decline, not all production growth has stagnated. Permian gross gas production continues to tick higher as highlighted in the chart below.

However, until Kinder Morgan’s Permian Highway Pipeline enters service in early 2021, Permian gross gas production will fail to translate into material gains in dry gas production. Waha futures imply negative pricing is on the horizon for Permian producers this summer. Additionally, further legal challenges possibly delaying Permian Highway pipelines’ in-service date could leave the natural gas market short supply next winter should a cold winter strike North America and boost demand. For more on BTU Analytics’ outlook on Henry Hub Natural Gas Pricing see BTU Analytics’ Henry Hub Outlook.