US LNG demand hit a new high this week. Daily feedgas deliveries to LNG facilities exceeded 10 Bcf/d for the first time. The record-setting levels are made even more impressive on the heels of summer with daily deliveries falling as low as 2.2 Bcf/d. Despite this recovery, the response of US LNG during the COVID-19 pandemic has highlighted the role of the US as a swing supplier of LNG in the global market, which could portend trouble in the future. Today’s Energy Market Insight will look at how other major LNG producers fared this summer compared to the US, and what that might mean for US LNG demand moving forward.

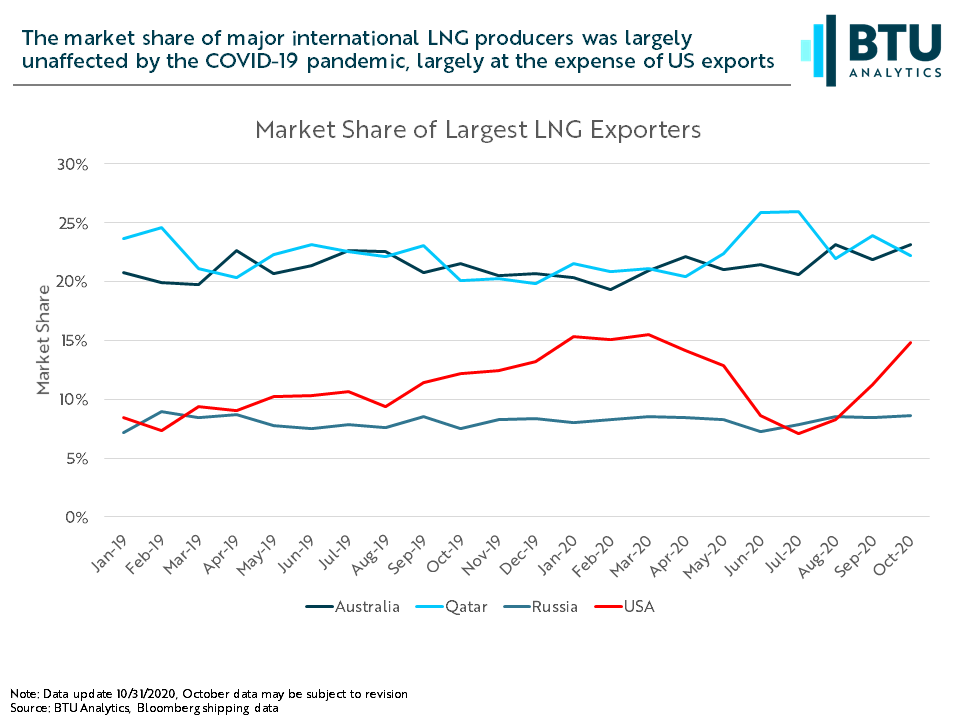

Global LNG exports are dominated by four countries: Australia, Qatar, Russia, and the United States. Together they averaged over 60% of total exports in 2019 and have averaged 65% in 2020 thus far. However, while the total market share for the big four fell only marginally during the summer, the US felt a disproportionate impact compared to the other countries. In July, the lowest month for US LNG exports, the US made up just 7% of global exports, a 54% decline compared to March. In comparison, Australia and Russia maintained their market shares at 21% and 8%, respectively, while Qatar increased its market share to 26%.

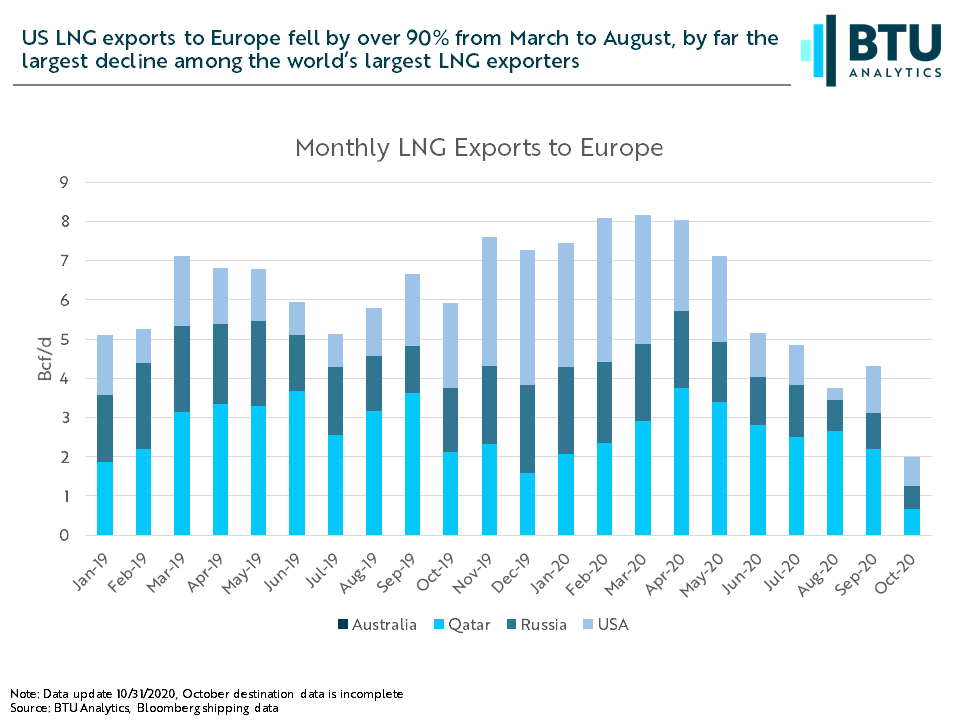

The divergent trends in market share lend support to the idea that the US is the swing supplier for global LNG. It is further reinforced by the dynamics observed over the summer in the world’s two largest demand regions: Europe and Asia. As BTU Analytics previously examined back in April, Europe served as a major demand sink in the winter of 2019/2020, increasing imports by 33% winter over winter. While both Qatar and Russia were able to capitalize on this increase in demand, the main beneficiary was the US as it increased exports to Europe by over 2 Bcf/d on average compared to the previous winter. However, as demand fell due to the COVID-19 pandemic, the US was also the hardest hit, falling to just 0.3 Bcf/d in August, a decline of 91% compared to March levels. While Russia and Qatar also experienced losses, 60%, and 30%, respectively, the US was clearly at a relative disadvantage which could prove problematic moving forward.

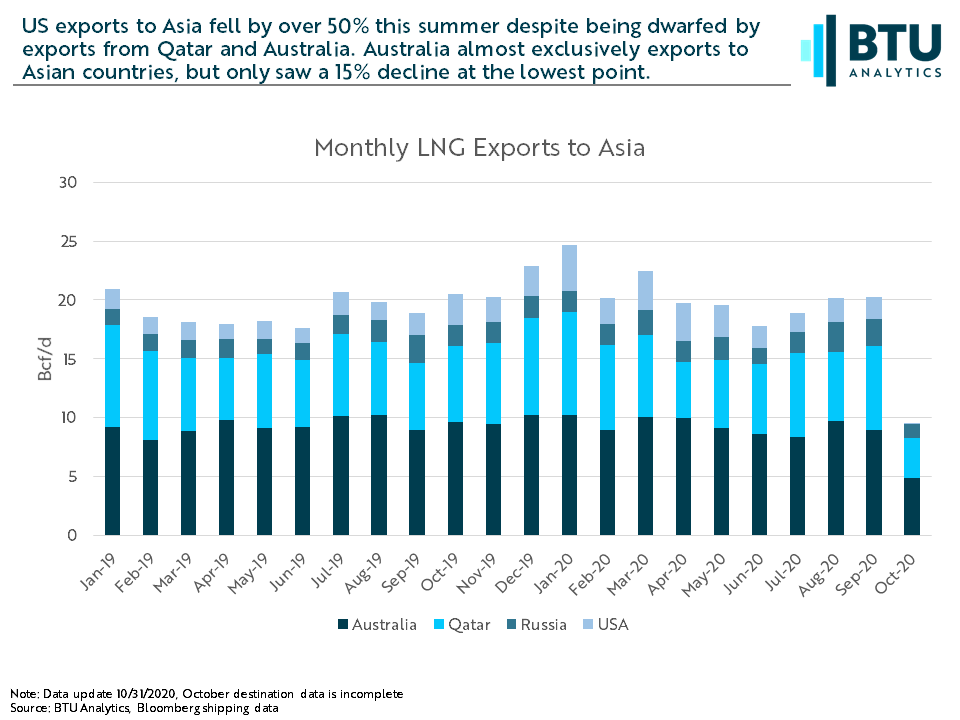

A similar dynamic is evident in Asia, although to a lesser degree. As in Europe, US exports to Asia increased significantly in winter 2019/2020 peaking at over 3.85 Bcf/d in January 2020. US exports then fell significantly over the summer declining by 53% at the lowest point compared to March export levels. At their lowest point, Russia and Qatar experienced declines of only 36% and 34%, respectively. The Asian market is further complicated by the presence of Australia, one of the two largest exporters in the world, which almost exclusively exports LNG to Asia. While Australian exports fell by 15% to 8.3 Bcf/d, it still accounted for over 40% of Asian supply.

As evidenced by current LNG feedgas deliveries, US LNG is fully capable of being a significant source of natural gas demand in the US. However, as the effects of the pandemic have illustrated, US LNG is unlikely to be as resilient as its global counterparts when demand, and pricing, collapses in Europe and Asia. Moving forward, US LNG could see significant volatility, especially if strength in Henry Hub pricing eliminates netback opportunities for US producers. For more on BTU Analytics’ outlook for US LNG, request a sample of our monthly Henry Hub Outlook report.