The pace of inbound questions to BTU about the gas market has been up in recent months with callers interested in discussing gas market dynamics in Oklahoma, Northern Louisiana, Rockies, and Appalachia. Our response to each of these requests are, ‘yes we can talk about the play of interest, but we are going to have to talk about the Permian as well, which demonstrates the expanse and extent of the current levels of activity in the Permian and subsequent impacts to the U.S. gas market. In this Energy Market Commentary, we will show in three charts why what happens in the Permian reverberates throughout the industry. These charts are 1) depth of inventory, 2) Permian’s capture of U.S E&P CapEx and 3) Permian gas growth vs. total U.S. demand growth.

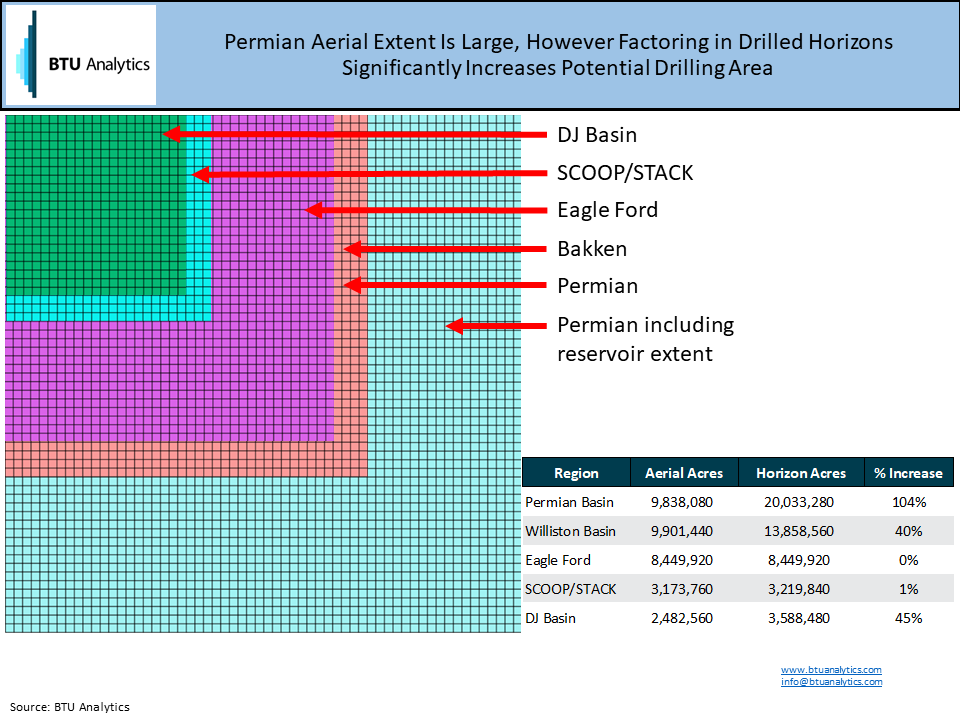

First, the geographic size advantage of the Permian is impressive, however, on an aerial acreage basis, it ranks up there with the Bakken and Eagle Ford. But when multiple drilling horizons are considered, even by the most conservative estimates of horizons that could potentially be developed, this doubles the size of potential developed “horizon acres” for the region, putting it in a league of its own in relation to other major plays as shown above. Extensive inventory based on aerial and horizon acreage, in addition to favorable Permian breakevens (which we have covered in a previous post), means that capital for infrastructure and drilling flows more freely to the Permian, allowing it to continue to disrupt North American gas regional balances for the long-term.

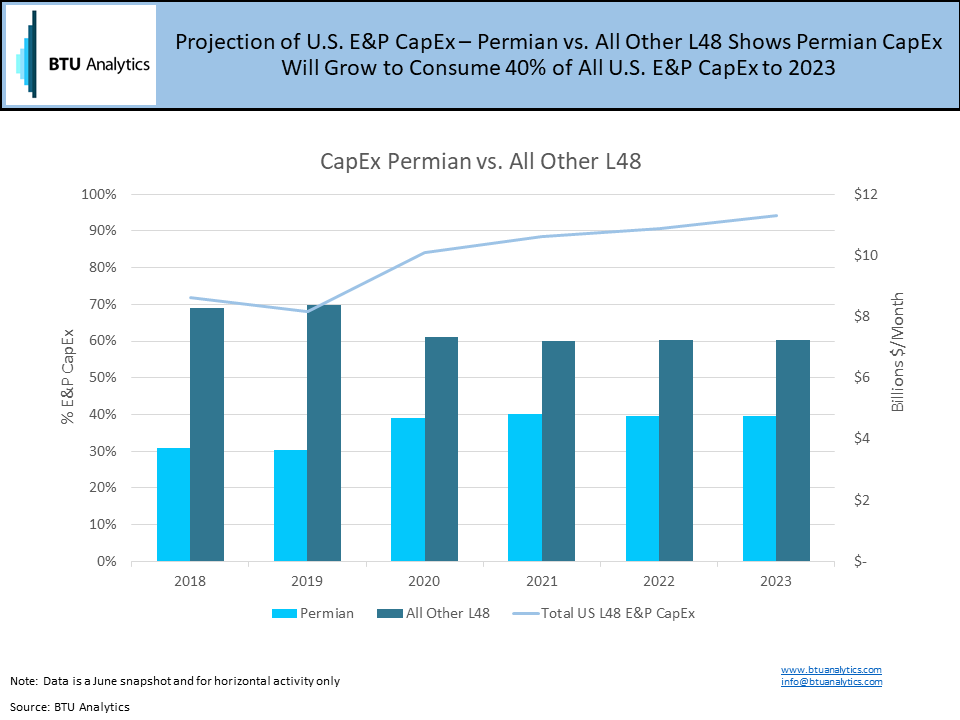

Second, the Permian is increasingly consuming a larger slice of total U.S. E&P CapEx. BTU estimates that by 2020 the Permian will grow to represent 40% of U.S. E&P CapEx (based on BTU Analytics’ Cash Flow Tool looking at horizontal activity only). More Permian CapEx means more activity and production growth relative to other plays.

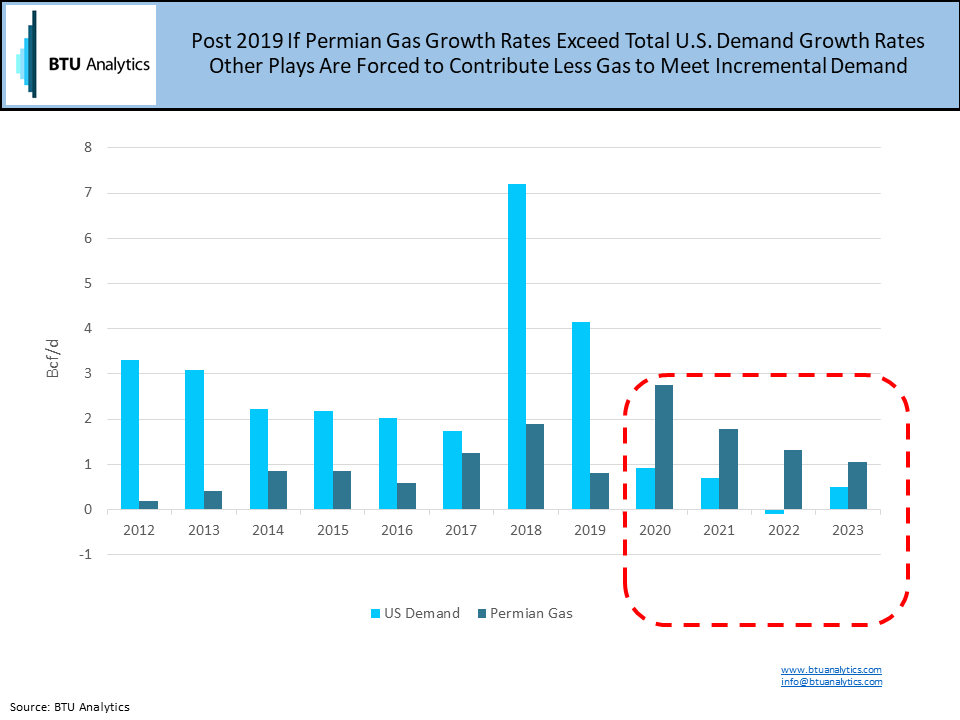

Adding insult to injury, BTU’s forecast calls for Permian gas growth to outpace US Demand growth from 2020 – 2023. This means that all else equal, other plays will need to decline to accommodate Permian gas growth. Baring a major WTI price correction, Permian associated gas is going to impact all gas basins for years to come. To follow these trends more closely request more information about BTU Analytics’ Upstream Outlook.