After years of downspacing in the Permian, E&P companies are beginning to pursue increased well spacing to resolve the “parent-child” problem as detailed by the WSJ early last month. Despite claims of increased performance from closely packed wells, performance has been less than promised, leading some to concerns over the potential impact of a glut of underperforming wells on the outlook of the Permian. In today’s Energy Market Commentary, BTU Analytics looks at the well spacing trends and who has DUCs that may be impacted by the change in Permian spacing trends.

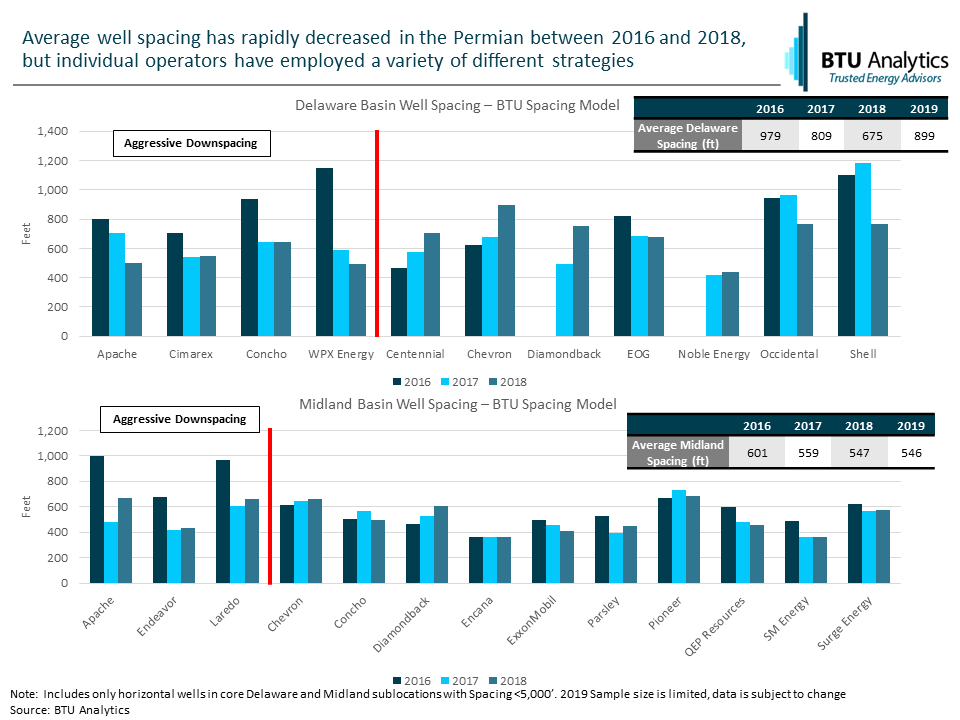

Beginning in 2017, Permian operators began aggressively downspacing in both the Delaware Midland basins. In the Delaware, average well spacing fell from 979 feet in 2016 to 809 feet in 2017 and 675 feet in 2018. A similar trend occurred in the Midland albeit at a much smaller magnitude. Average Midland spacing fell from 601 feet in 2016 to 559 feet and 547 feet in 2017 and 2018, respectively. However, while spacing across the Permian decreased, spacing strategies were very diverse among individual operators, as illustrated in the chart below. In the Delaware, Apache, Concho, and WPX Energy were far more aggressive in pursuing tighter spacing than other top operators. In the Midland, tighter spacing was driven primarily by Apache, Endeavor, and Laredo Petroleum. For more on BTU Analytics’ methodology on spacing, please see our September Upstream Outlook.

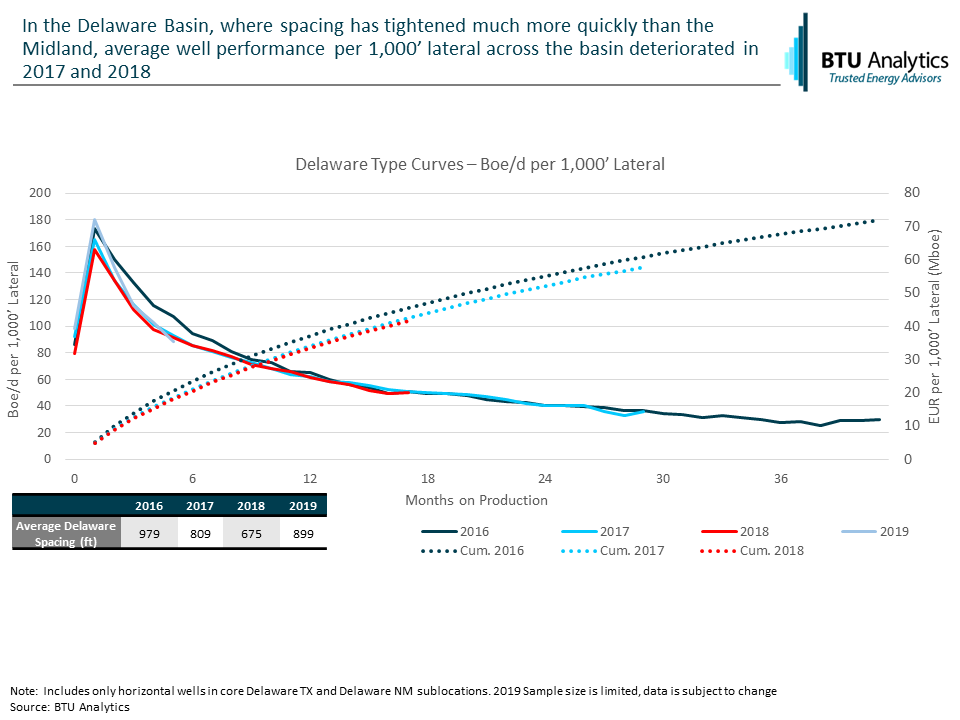

While tighter well spacing was expected to help boost Permian’s well performance, the results from wells drilled in 2017 and 2018 have been less than promising. In the Delaware, where well spacing has tightened much quicker than in the Midland, productivity on a per lateral foot basis declined across the basin in 2017 and 2018 relative to 2016. As shown in the graph below, initial production rates per 1,000’ lateral were 6% lower in 2017 and 10% lower in 2018 compared to 2016. In addition, EUR per 1,000’ lateral after 12 months of production is 9-10% lower in 2017 and 2018 wells compared to 2016 wells. However, while productivity per lateral foot has declined, well productivity has actually increased as longer lateral lengths have helped offset the declines in productivity per lateral foot.

The deterioration of productivity per lateral foot has prompted companies to begin moving back to wider well spacing. In their 2018 4Q earnings call, Laredo Petroleum acknowledged the weaker performance of their tighter spaced wells and announced they would move to wider spacing going forward. As companies return to increased well spacing, it raises the question of what to make of the current inventory of DUCs that were drilled using the tighter spacing regimen.

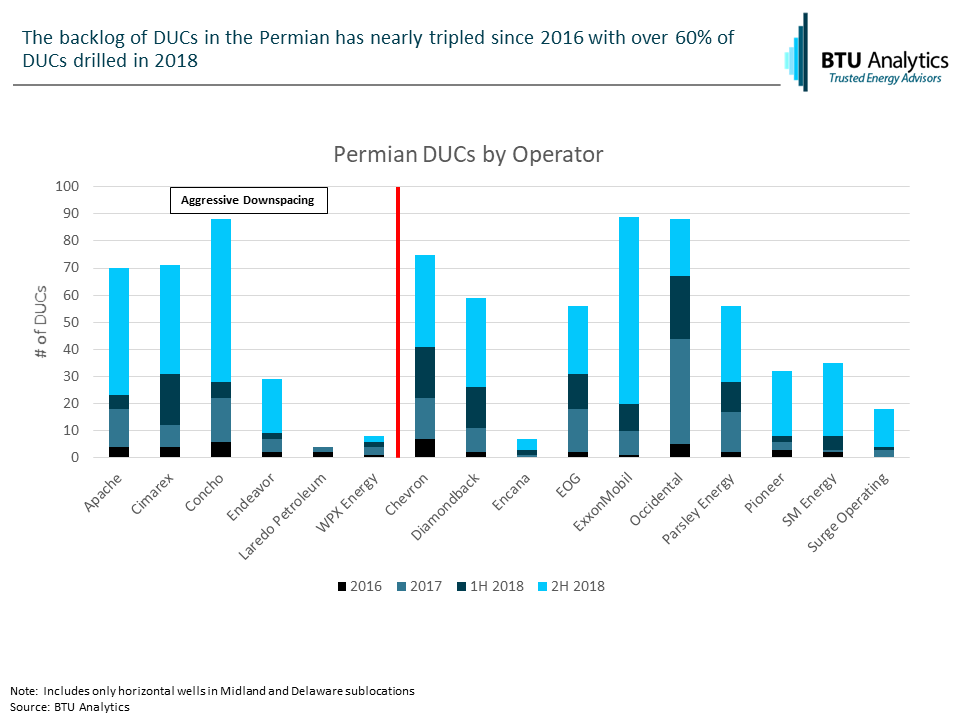

In the past two years, the Permian has added over 1100 DUCs, nearly tripling total DUCs from 600 at the end of 2016 to almost 1800 at the end of 2018. Of these, over 60% were added in 2018 when average well spacing was the tightest. This has raised concerns that the large backlog of DUCs may be primarily composed of potentially under-performing wells. In the chart below, BTU Analytics looked at DUCs by operator for some of the top operators in the Permian. While some operators who aggressively downspaced saw an increase in DUCs (Apache, Cimarex, Concho), others had few, if any DUCs added in 2018 (Laredo, WPX). In addition, most 2018 DUCs were drilled in the second half of 2018. This likely indicates that this increase was tied to the increased pace of drilling activity in 2018 rather than the impact of poor well performance results.

Additionally, operators in the gassier portions of the Permian such as Cimarex have seen their DUCs increase as percentage of the wells drilled. Indicating that some of these operators may have held off completions in the weak natural gas and oil pricing environment at the end of 2019. So while operators are shifting strategy on spacing for new development, it seems likely that as operators cut rigs from the field, the DUCs already in place will get worked through to help meet production guidance while spending less money on drilling.

For more on BTU Analytics’ DUC forecast and drilling activity in the Permian, request a sample of our US Upstream Outlook and our E&P Positioning Report.