A few weeks ago, BTU wrote a piece on the possible impacts of a successful TransCanada Pipeline Open Season, which was offering Canadian producers a potential opportunity to lock in reduced tolls to the Midwest and Dawn Hub markets in an attempt to regain share in those markets. Earlier this week TransCanada announced bid volumes were insufficient to continue forward with the proposal. Reports were that there was push back on the price not being competitive enough for such a long contract length (10 years), and despite the option of a 5 year contract also being offered, the new fixed price toll proposal has been halted. What does this mean for moving natural gas out of Canada?

Low priced natural gas from the Marcellus and Utica has been steadily displacing Canadian imports to Northeast markets, and without the lowered TransCanada toll proposal, the long-term trend is unlikely to reverse dramatically. While exports to the US increased through 2016 due to full gas storage in Western Canada and a depressed AECO price, BTU expects exports to the US to be under pressure even as Western Canadian production falls over the next five years.

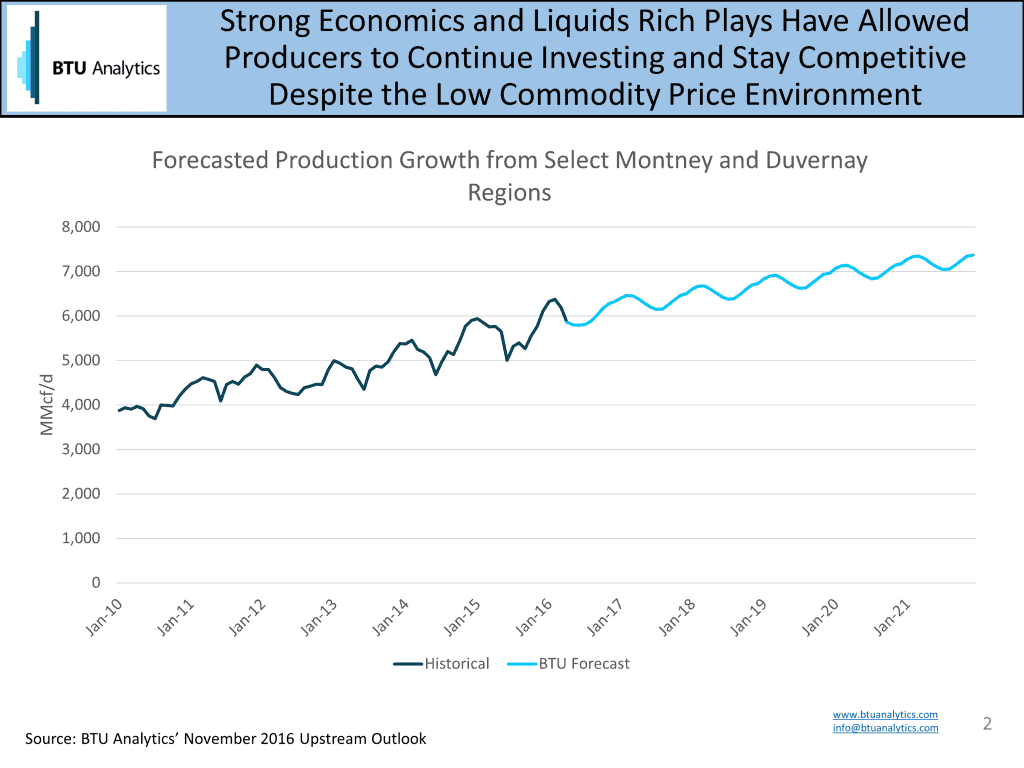

The production landscape in Canada has seen a rush to unconventional development not unlike the change in the US. Conventional development in Alberta, Saskatchewan and Manitoba, and eastern Canada have all seen production declines, and shifting activity and capital investments indicate that production wouldn’t rebound from these regions even with increased commodity prices. Production from the Montney and Duvernay has helped to offset declines in other areas as producers in these plays pushed the boundaries of well productivity and cost control in the low price environment. Producers such as Seven Generations (TSE: VII) and Encana (NYSE: ECA) have touted supply costs that rival the low cost gas from the Marcellus and Utica, and continue to grow production.

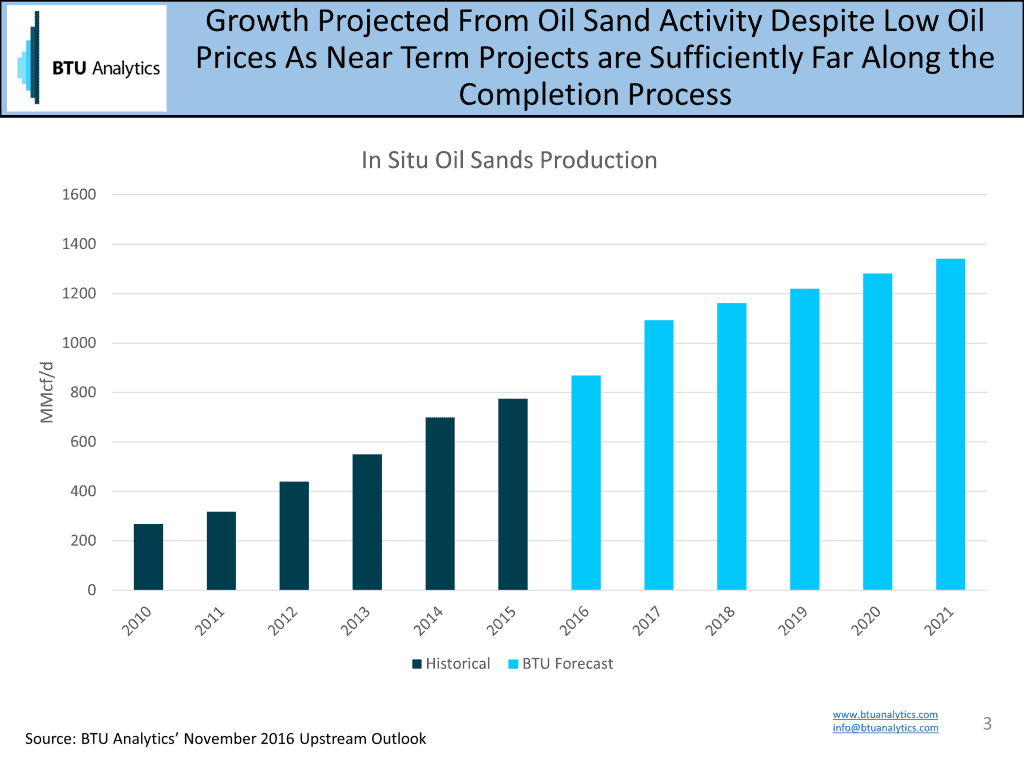

But even if Canadian natural gas production remains fairly resilient in the near term, changing natural gas flow patterns could have reverberations up North. The Midwest and Dawn markets will face increased pressure as new projects increase connectivity between these markets and the Marcellus and Utica. Canada expects modest demand growth from the residential/commercial and industrial sectors, but the Oil Sands are seen as the only major source of incremental gas demand on the horizon. Both mining and in situ oil sands activity draw on natural gas to provide process heat and upgrade crude bitumen to synthetic crude oil. Oil sands production growth is driven primarily by new projects coming online and bottleneck improvements on existing plants. While low oil prices may deter projects in the early stages of planning, BTU Analytics expects those under construction or near the end of the planning stages are likely to still move forward.

LNG exports remains in question for Canada as no proposed projects have been able to reach a final investment decision. While LNG could provide a much needed demand source for Western Canada, the earliest an export terminal could be completed is still 4-5 years out.

So what choices does this leave for Canadian producers that want to significantly grow production? One option is to head for the US Gulf Coast. Seven Generations announced in their 3Q earnings that they have contracted capacity on a 2-year term along NGPL from Chicago to the Gulf Coast. Access to the US Gulf Coast could be a key differentiation for certain Canadian producers, but the value of that strategy will depend on the pace of Marcellus infrastructure buildout (Rover and Nexus) and demand growth in the US.

For more information on BTU’s views on Canadian market upstream dynamics, request more information on our Upstream Outlook service.