Many US independent E&Ps have begun generating positive free cash flow in 2018, crediting capital discipline, operational efficiencies, and, perhaps most importantly, higher crude prices. The rise in oil prices over the past year has many drivers, but the largest has been from the agreement between OPEC and many non-member countries like Russia (together OPEC+) to cut production and rebalance global supply and demand. Tomorrow OPEC+ is meeting in Vienna in part to discuss a potential increase in production before scheduled cuts are set to expire at the end of this year. Russia and Saudi Arabia reportedly back a 1.5 MMb/d increase, while OPEC members as a whole could compromise and agree on a staggered 300-600 Mb/d increase. Because of this, we’ll discuss how these potential OPEC production increases could affect global balances, and therefore pricing.

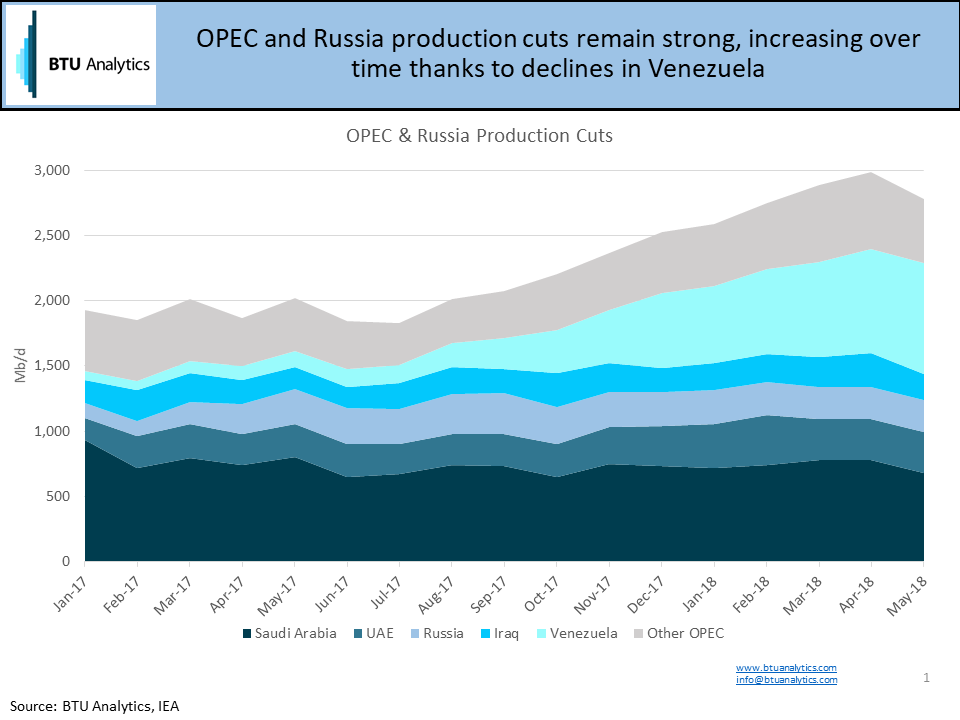

First, let’s take a look at the current progress of the cuts. The chart below shows the decline in production versus October 2016 levels for Russia and the OPEC member countries that agreed to production cuts, based on IEA data. Since the cuts began in January 2017 compliance has been high, which is well documented. Yet not all production that has been lost can be easily turned back on. Saudi Arabia, Russia, the UAE, Kuwait, and Iraq have spare capacity to bring production back online, but declines in production from Venezuela, which totaled 850 Mb/d in May, are driven by the country’s economic and political crisis and are unlikely to return.

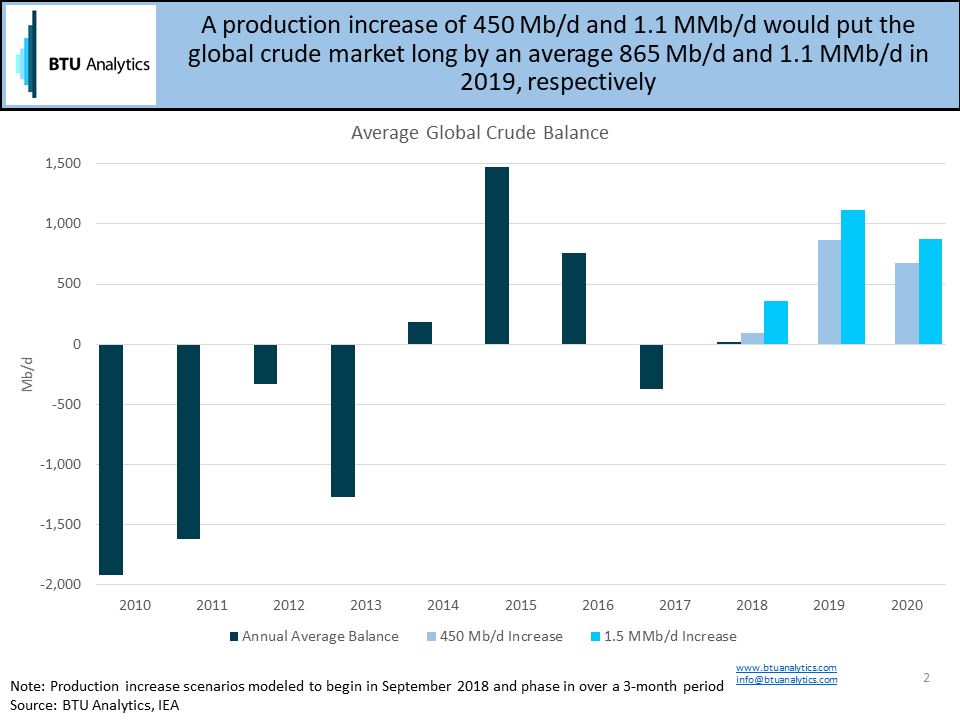

These quotas have rebalanced a global crude market that was long an average of 750 Mb/d of supply in 2016. As OPEC+ begins to think about winding down cuts, how could each scenario affect the market fundamentals? The chart below shows the annual average supply and demand balance for the global crude market for various scenarios. In our Oil Market Outlook, published this week, we currently model that production cuts will be wound down over several months beginning in January 2019 with the global market roughly balanced for 2018 and long in 2019 as US and Canadian production continue to rise. If OPEC agrees to increase production at the midpoint of the 300-600 Mb/d range beginning in September 2018, this imbalance is pulled forward slightly, causing global supply to outweigh 2018 demand by almost 100 Mb/d and 2019 demand by 865 Mb/d. Increasing production by the full 1.5 MMb/d, effectively unwinding the majority of current production cuts, would pull the average annual supply and demand imbalance up to 355 Mb/d in 2018 and more than 1.1 MMb/d in 2019.

The other half of the balance, global crude demand, is very important in these assumptions. Currently, we forecast global demand at an average 99.2 MMb/d in 2018, which is up 1.4 MMb/d over 2017. To balance the market in 2019 with a 1.5 MMb/d production increase, demand would need to increase by 2.7% (2.72 MMb/d), though we currently only model a 1.6% (1.61 MMb/d) increase globally.

While we have questions whether the coalition of OPEC and non-member nations have the spare capacity to ramp fully to a 1.5 MMb/d production increase, an increase anywhere near that level could send markets down a path away from the balance we’ve seen so far in 2018. We will certainly be watching for OPEC’s decision on production tomorrow. To see how we forecast these changes affecting Brent, WTI and regional US crude price points, request a sample of the Oil Market Outlook today.