The current US administration has set a target for 100% clean energy by 2035, with the goal of net zero carbon emissions by 2050. Oil and gas focused energy sector players, both global and US-based, have publicly announced commitments to net zero carbon emissions, with timelines ranging from the more conservative 2050 target to some truly ambitious ones, such as Antero Resources’ (NYSE:AR) goal of net zero scope 1 carbon emissions by 2025. One thing many of these announcements have in common is the need for carbon capture to play a role in meeting these goals. However, carbon capture and sequestration is prohibitively expensive right now, making it economically unviable at scale without an additional catalyst. Enter the 45Q. Named after its location in the US tax code, the 45Q is a tax credit earned for every MT of carbon dioxide (CO2) sequestered underground. While this sounds simple, like everything else in the US tax code, plenty of nuance lies therein. Today’s Energy Market Insight will give an overview of what the 45Q tax credit is and how it is changing.

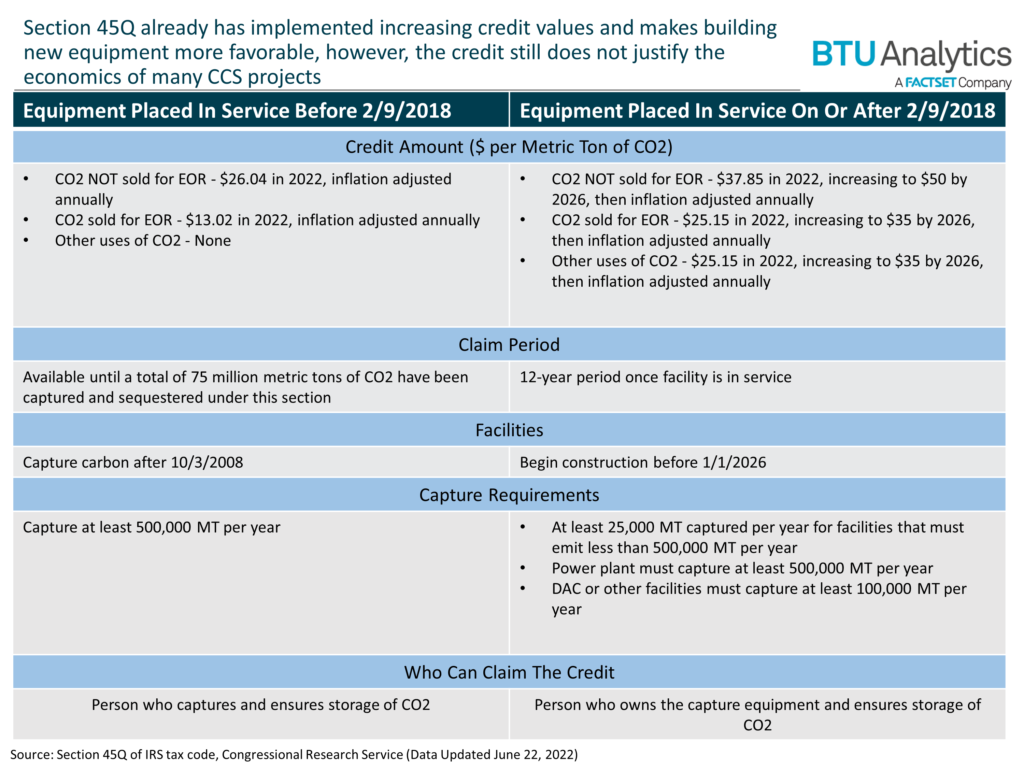

The above table gives an overview of the more important aspects of the credit. Notice different rules and credits are given to equipment based on its In-Service Date (ISD), with Feb. 9, 2018 being the key date. Across all projects in this category, equipment placed into service before Feb. 9, 2018 gets a reduced credit and is no longer eligible for the credit after a total of 75 million tons of CO2 have been captured. Current estimates from the IRS and other congressional research groups indicate around 73 million tons of CO2 have been captured in this way already. However, for equipment placed in service after that February 2018 date, the credit is much more generous, and can be claimed for a period of 12 years.

There have also been recent proposals to extend and enhance the credit, which are still going through the legislative process. Some of the proposed changes include extending the tax credit to 2030, increasing the value, and even targeting Direct Air-Capture (DAC) projects, which would receive a credit of $180 per metric ton of CO2 sequestered. If some of these changes make their way to fruition, one could expect to see an increased pace of carbon capture projects coming online. Current consensus indicates most carbon capture projects would need a credit of around $80-100/MT to become economic.

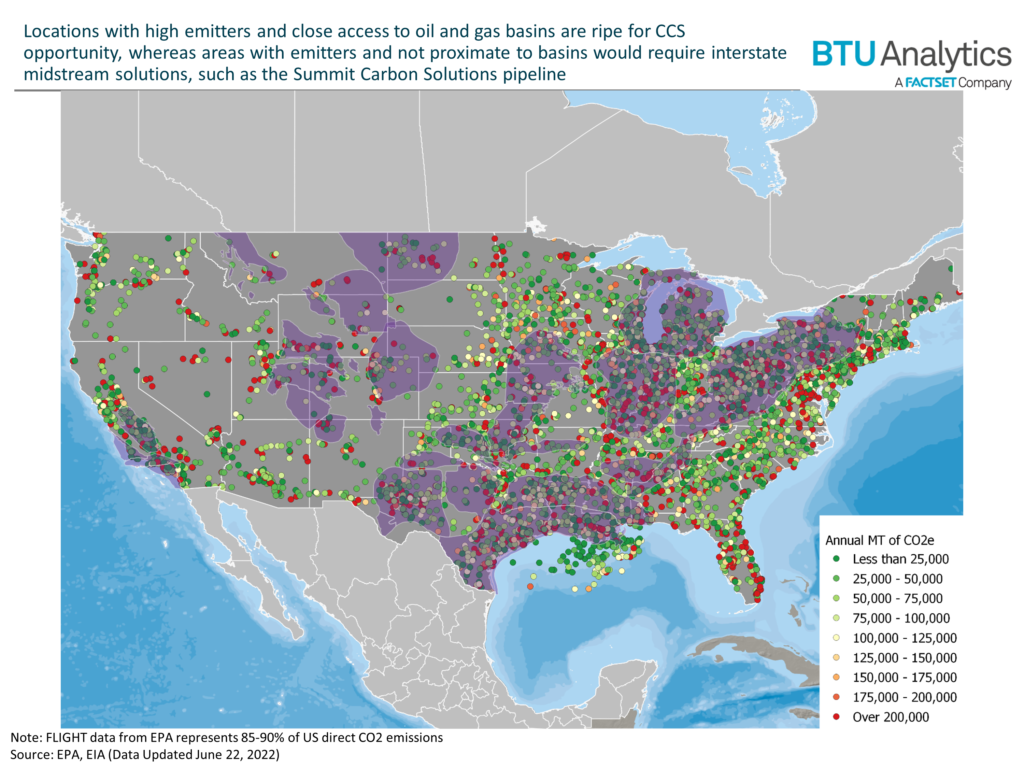

Should incentives align, where could development happen? Below is a map of US scope 1 direct carbon dioxide emissions, overlaid with major onshore shale basins in the US.

The most obvious places that could see a big boom in development are in Texas and along the Gulf Coast. Not only are there many large industrial and petchem emitters located there, but there is ample pore space available for storing the CO2. Regardless of whether you sell the CO2 for use in EOR or store it underground, the CO2 must still be sequestered underground in order to claim either version of the credit, which is a requirement explicitly stated in the 45Q language. Refiners that utilize CCS would also lower the carbon intensity of fuels they produce, which opens them up to other forms of financial gain, such as Low-Carbon Fuel Standards (LCFS) credits in California. Another trend to watch is what approach industrial emitters along the Atlantic seaboard and in the Midwest consider for capturing and sequestering carbon. These areas have plenty of carbon emissions ripe for capturing, but storage would require extensive networks of interstate CO2 pipelines, a hurdle that those in the oil and gas industry know is significant.

Ultimately, many potential developers of CCS projects have indicated the 45Q credit needs to be higher to make development feasible, and, even then, some developers would need additional changes, such as direct payment. Despite these obstacles, companies are exploring CCS projects, hoping to advance the technology and be the first movers in the space, should financial incentives improve.