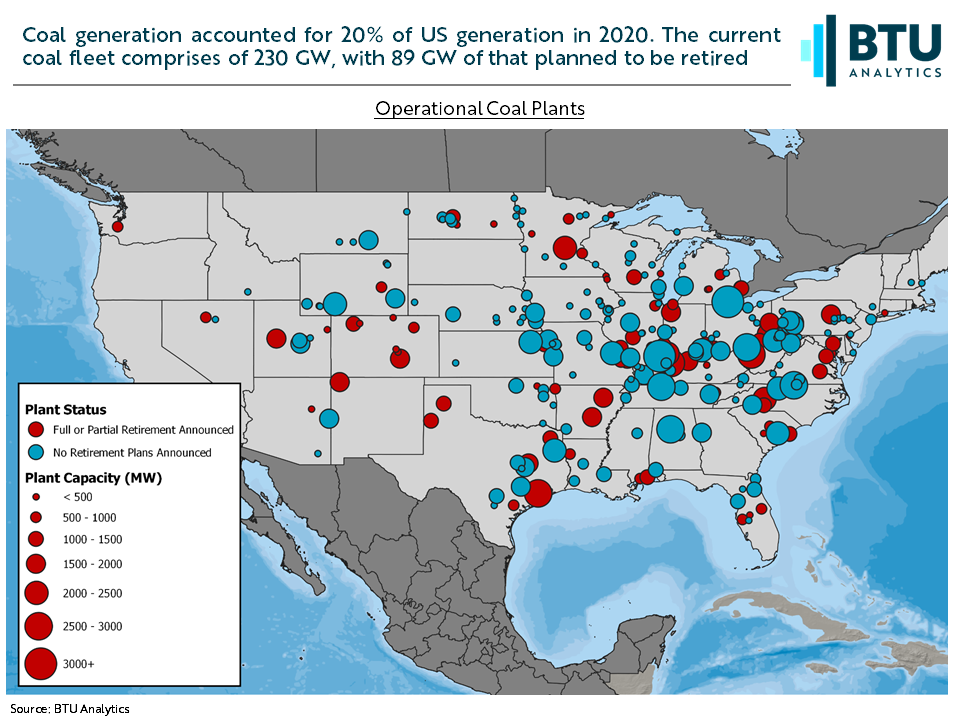

In 2020 coal generation accounted for 20% of the US’ overall generation mix. This was down from a third just five years earlier. While there are many factors leading to why any power plant retires, today, we will look at how renewables development has either front ran or backfilled retiring coal plants.

First, let’s look at US’ current fleet of about 600 coal-fired units. These units total just over 230 GW, with 185 units totaling almost 89 GW of that capacity set to be retired. The map below shows the US’ currently operational fleet of coal plants with red circles signifying plants that have either announced partial or full retirements. If you are interested in seeing the coal fleets’ top emitters see our recent Energy Market Insight

Broadly speaking, renewables, along with natural gas-fired generation, have pushed overall marginal costs down, lowering power prices and coal generation revenue. Coupled with environmental regulation and state/utility emissions targets, retrofitting or maintaining emissions control equipment, mounting coal ash liabilities puts a strain on already struggling plants.

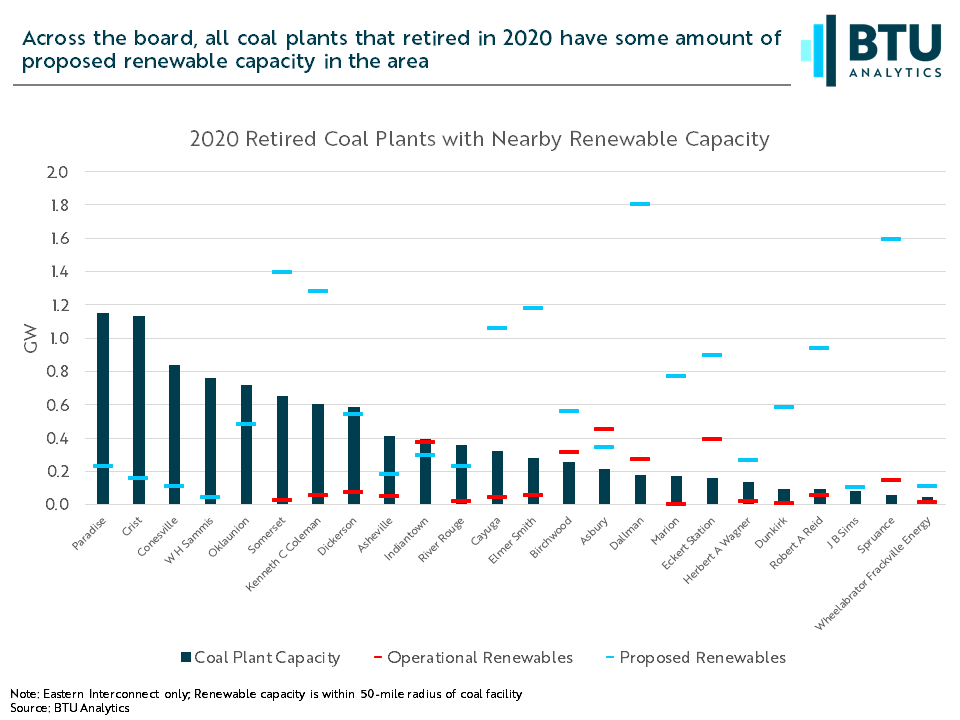

The following graphic shows the 10 GW of coal capacity that was retired in 2020 along with operating and proposed renewable capacity in their vicinity. Across the board, all the plants that retired in 2020 have some amount of proposed renewable capacity in the area as measured by radial analysis. Depending on the region of the country, this could be an attempt to utilize newly freed up infrastructure and mitigate potential interconnection costs for renewables. Only a handful of plants had meaningful operational renewables capacity in the area when it retired.

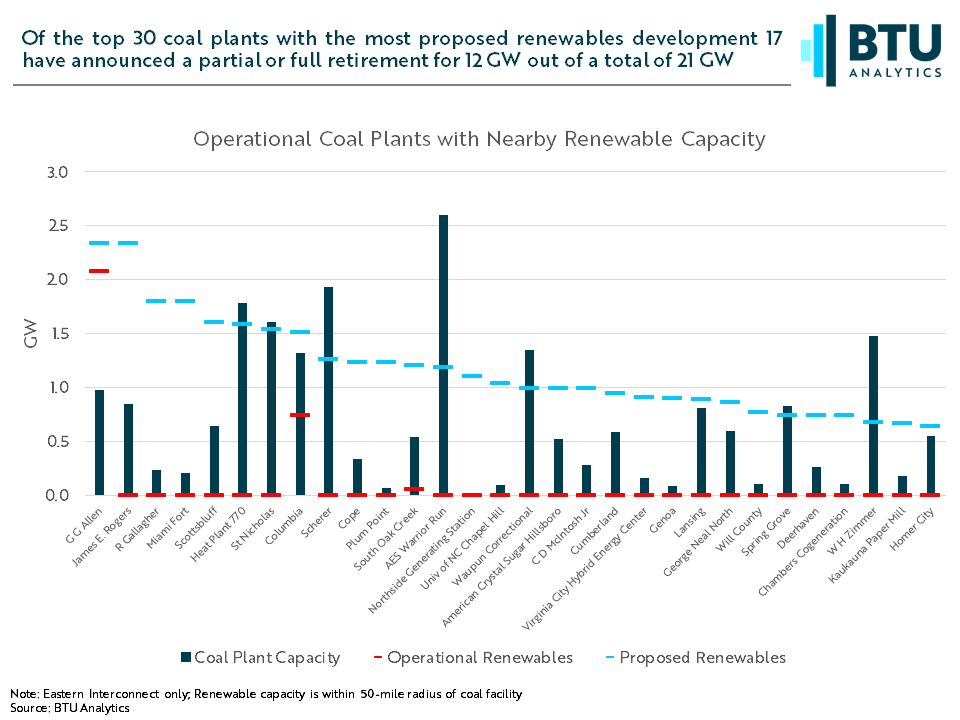

We can take this same approach but now look at the 292 coal plants that are still in operation. The graphic below shows the top 30 coal plants with the most proposed renewable capacity in the area. Of the plants listed below, 17 have already announced plans to fully or partially retire, totaling about 12GW of a total 21 GW.

Like we mentioned earlier, increased renewable generation is just one factor to consider when identifying plants potentially at risk of retirement. Economic dispatch and transmission capacity between areas can mitigate the risk to having nearby competitors, so a large renewables presence in the area of a plant does not mean that plant will retire. However, it is difficult to find a silver lining, especially for plants that have a slow start-up time or are not able to economically ramp intermittent backfill generation.

If you are interested in digging in deeper, BTU Analytics Power View provides a comprehensive dataset of power plants, including proposed, existing, and plants with planned retirements. To see its complete offerings setup a one-on-one demo today.