Understandably, many of the headlines this winter have reported on the historic cold temperatures seen in the Upper Midwest and blizzard-like conditions from the recent bomb cyclone. If you’re not an avid skier or snowboarder, something that might have flown under the radar is this season’s above-average snowpack in the West. As temperatures warm, that snow will melt off and feed the West’s more than 50 GW of hydroelectric facilities, in turn affecting the amount of natural gas power burn we can expect in the coming months.

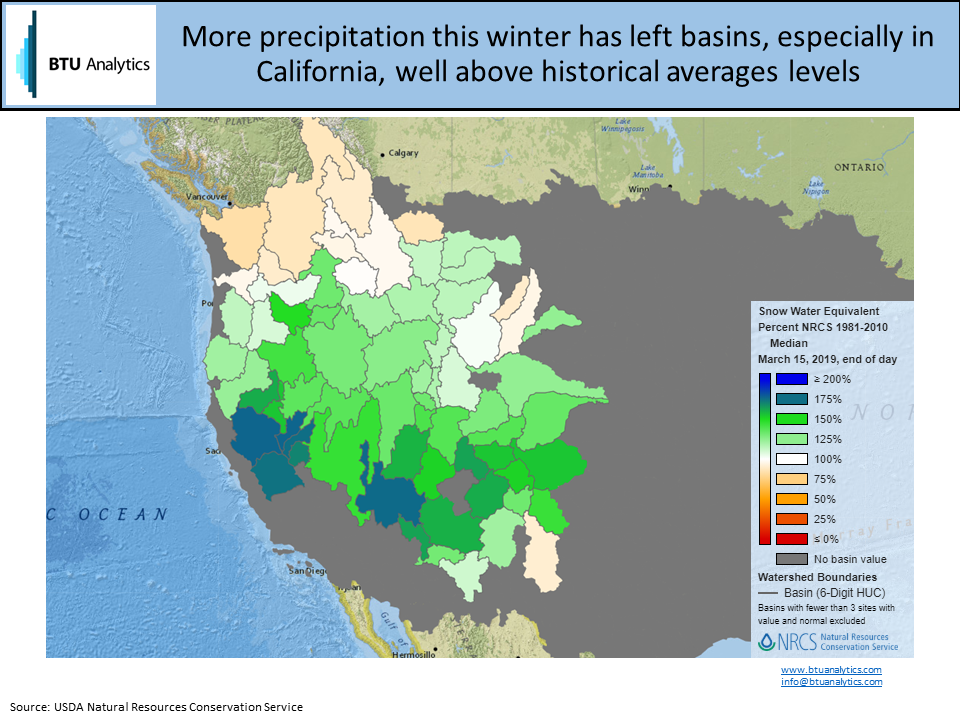

The USDA’s Natural Resources Conservation Service tracks weather station data in western states and aggregates that data up into the basins highlighted in the map below. As seen by the dark greens and blues, higher than normal precipitation this winter has left basins in California and the Southwest well above historic averages.

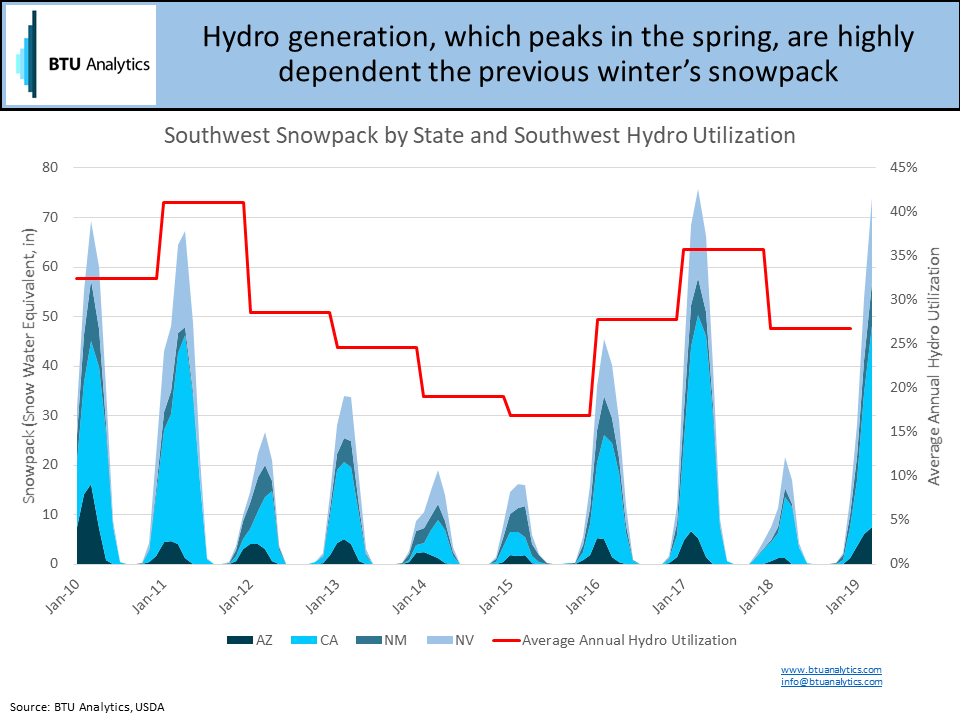

Although we are at snowpack levels seen just a couple of years ago, it is a drastic change compared to last year and a divergence from historic averages, as shown in the graphic below. Naturally, snowpack translates to higher hydroelectric generation levels, and hydro utilizations ebb and flow based on the previous winter’s snowpack levels.

In California, especially, additional hydro comes at the expense of natural gas fired power generation. In fact, when hydro generation was weak in 2014 and 2015, we saw natural gas deliveries to power plants in California reach highs of near 2.5 Bcf/d and as hydro returned in 2016 and 2017, natural gas deliveries dropped off to about 1.9 Bcf/d. Not all of that drop is attributable to hydro, but no doubt it played a role in driving down power burn demand.

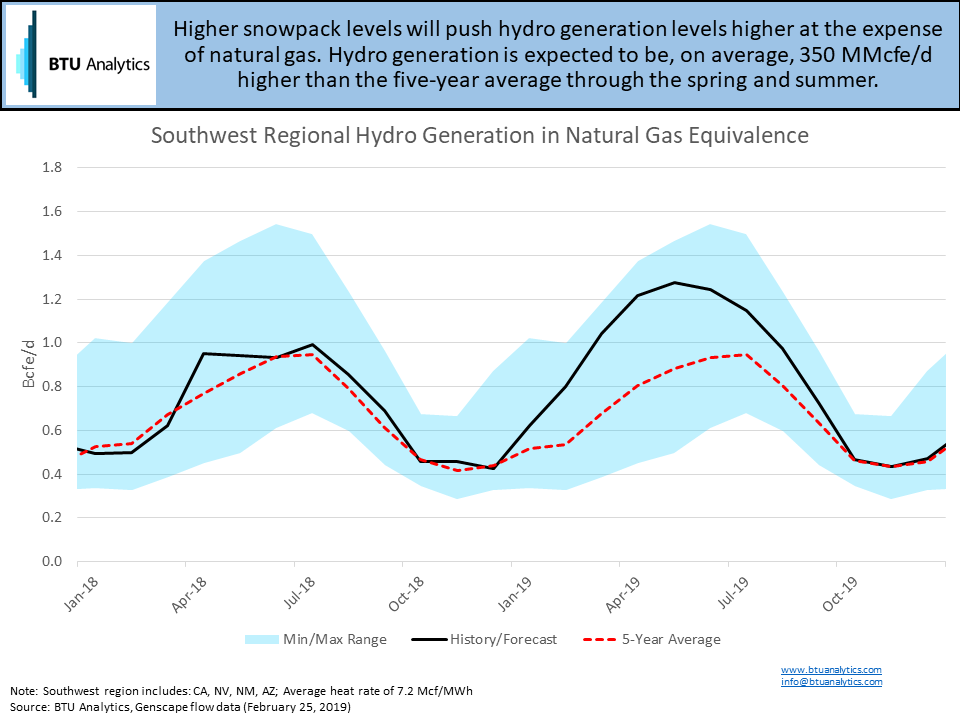

Looking forward, what can we expect from hydro generation in the coming months? Putting things in terms of natural gas power burn equivalent, in the Southwest, we typically see hydro generation hit lows in the winter of around 0.4 Bcfe/d and rise to a peak of close to 1.0 Bcfe/d in July, as shown by the red dotted line below.

However, higher than average snowpack will lead to a divergence from the normal, with about an additional 0.35 Bcfe/d of hydro generation expected throughout the spring and into the summer.

Beyond electricity markets, above average hydro generation has implications for the wider natural gas market. Currently, Southern California provides an end market for both Rockies gas (via Kern) and Permian gas (via El Paso and Transwestern). All else equal, less demand in the West means downward pricing pressure will be transferred back onto supply basins. Kern flows have shown resilience throughout the past regardless of hydro generation, so it is likely Waha pricing will feel the negative effects of increased hydro generation, as a potential route for Permian associated gas will be restricted.

For more on BTU’s power burn and natural gas pricing outlooks see the latest editions of the Henry Hub Outlook and Gas Basis Outlook.