Like many parts of the country, early summer heat pushed the Southeast power market to typical July and August peaks in May and June. As summer temperatures have dragged on, Southeast gas pricing has surged, with Transco Zone 4 basis reaching a premium of $5.05 on July 27th. While there are other drivers outside of the power sector pushing gas prices higher, will Southeast power demand continue to exacerbate the natural gas market or is relief on the way?

Today’s Energy Market Insight is an abridged excerpt from an upcoming report on Southeast power and natural gas markets that will appear in BTU Analytics’ 3Q 2022 Gas Basis Outlook.

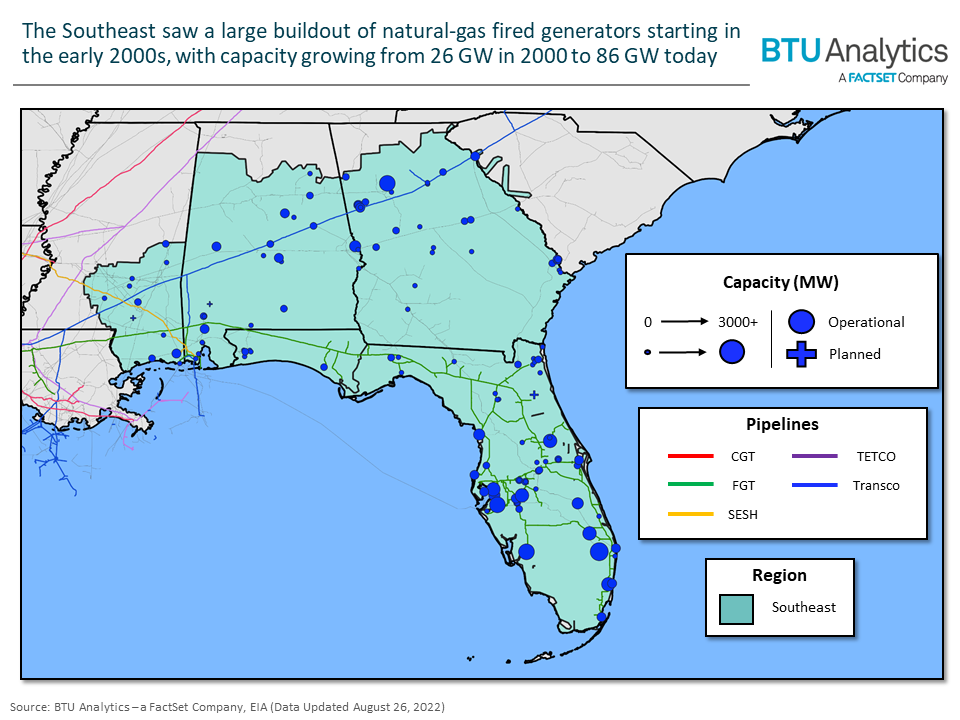

The Southeast (as defined by the region outlined below) has seen structural load growth over the past two decades as Americans have, on average, migrated from northern states to southern states. This coincided with a large buildout of natural gas-fired capacity that began in the early 2000s and continued into the early 2010s. As new natural gas plants came online and natural gas prices fell due to shale production, gas generation surged at the expense of coal, with regional coal-fired generation falling 70% since 2000.

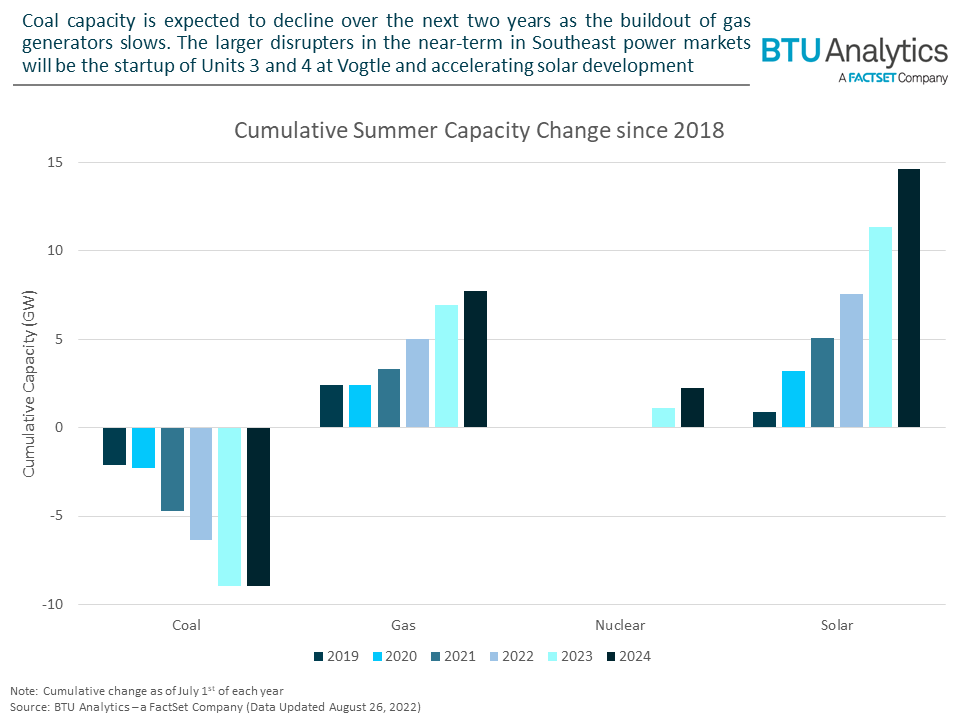

Also of note in the Southeast’s generation mix is the consistent production from the region’s 10 GW fleet of nuclear generators. This nuclear generation will increase soon, as Southern Company’s long-awaited 1.1 GW Vogtle Unit 3 received its approval this month to begin fuel loading and operations and is scheduled to come online in March 2023. The 1.1 GW Unit 4 has not received all its inspection approvals but is expected online by the end of 2023.

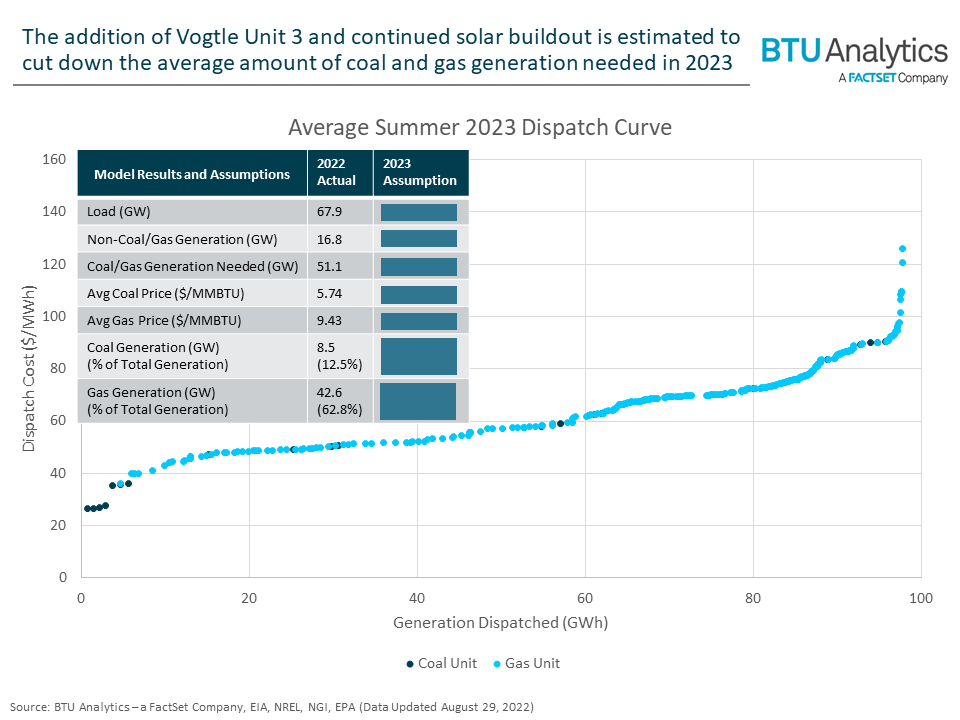

To build a regional dispatch model that highlights what generation is at risk, BTU combined the expected capacity changes above with regional utility load forecasts, expected capacity factors for non-coal and non-gas generators, and assumed coal and natural gas plant costs. The dispatch curve below shows the assumed ordering of natural gas (light blue) and coal (dark blue) units based on economics, with most economic units on the left to least economic units on the right.

Over the next two years, the commissioning of Vogtle Units 3 and 4 and an expected 7 GW of solar capacity will force natural gas and coal-fired generation down. In the medium to long-term, growing solar capacity will be the largest disrupter to Southeast power markets, as the three largest utilities in the region have all announced aggressive plans to grow solar generation in their most recent Integrated Resource Plans.

As stated above, today’s Energy Market Insight was an abridged excerpt from an upcoming report that will be published in BTU Analytics’ 3Q 2022 Gas Basis Outlook. To see the complete analysis of Southeast power and natural gas markets, contact BTU Analytics for a trial of the Gas Basis Outlook and the Power View.