Around two decades ago, the Barnett Shale kickstarted the shale revolution by becoming one of the first areas to employ the practice of combining horizontal drilling with hydraulic fracturing, thus allowing operators to access natural gas from “tight” source rock. Operators and capital have since moved across the globe to plays like the Marcellus and Haynesville, which have now become even more productive than the Barnett. However, infrastructure bottlenecks and inventory depletion in core plays could re-spark investment in other areas like the Barnett. Today’s Energy Market Insight is an excerpt from a report that appeared in the recently published August 2022 edition of BTU’s Upstream Outlook, and while the original analysis discusses the Barnett’s recent refrac activity, existing infrastructure, and remaining inventory, today’s Insight will focus on the historic gas play’s economics and remaining inventory.

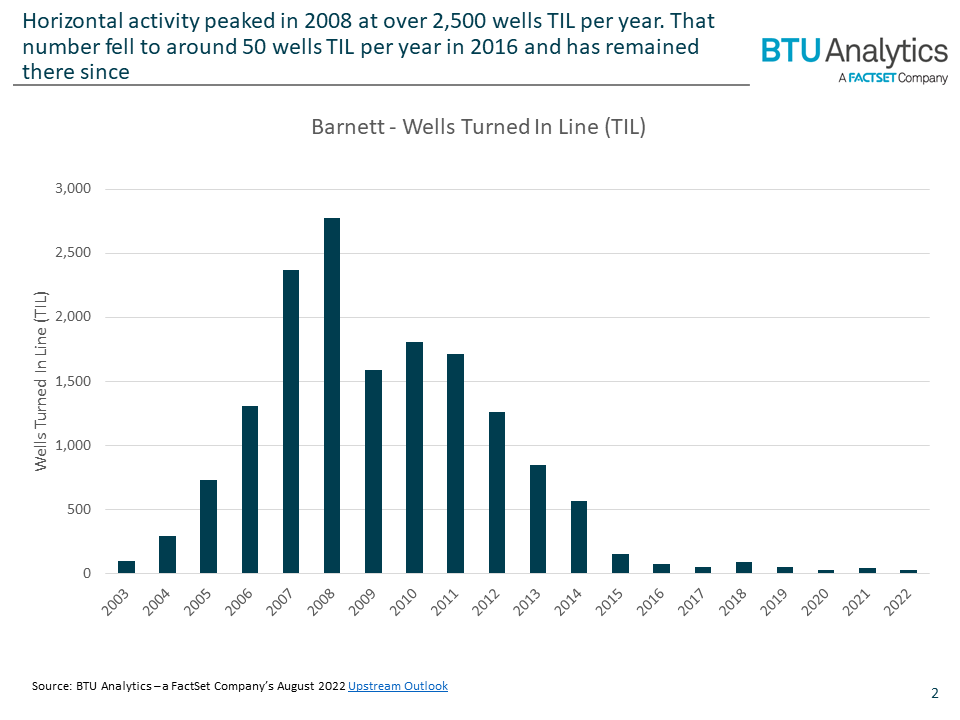

Horizontal drilling quickly took over the Barnett in the early-2000s. So much so that in 2008, activity in the North Texas gas play peaked at over 2,500 wells turned-in-line (TIL) per year, making it the largest producing shale play in the US. However, the Haynesville and Marcellus quickly became more attractive, and within five years, activity in the Barnett fell significantly. Today, activity in the Barnett hovers around 50 new wells TIL per year, a level that has gone largely unchanged since 2016.

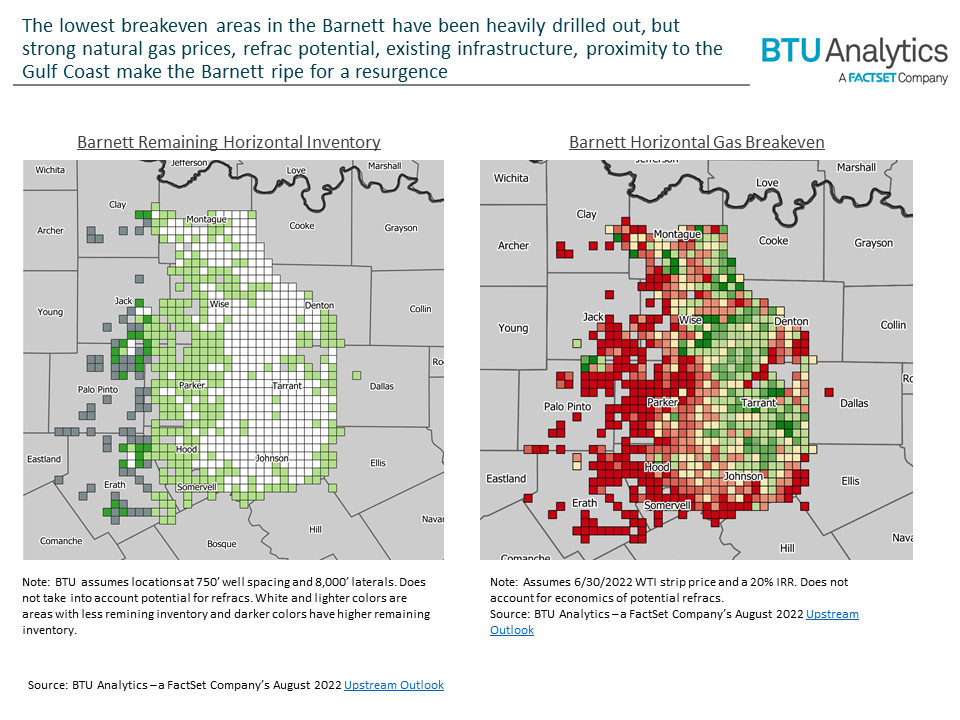

Despite the Barnett having been drilled extensively over the years, undrilled acreage does remain. To understand the future potential contribution of Barnett resources at various price points, BTU paired undrilled acreage with historical well-level breakeven economics, similar to what BTU publishes for key shale plays each month in our Oil & Gas – Economics View, to develop remaining inventory estimates by breakeven for the Barnett.

The map above (left) shows remaining drilling locations with white boxes being the areas with the fewest locations and dark green boxes being the areas with the most. In the other map above (right), dark green grids indicate breakeven economics below $4/MMBtu and dark red boxes indicate breakeven prices of at least $9/MMBtu based on a 20% IRR. By pairing the map of remaining locations with a breakeven map, BTU is able to estimate remaining new drilling locations by breakeven. Wells at the border of Wise and Denton counties, as well as in Tarrant and Johnson counties, have the lowest breakeven prices, but the acreage has been largely drilled out. While significant undrilled locations remain in other counties, such as Parker, Hood, and Somervell, gas prices would need to increase in order for them to be considered economic.

Based on economics for new wells, long-term pricing needs to be higher to incentivize a resurgence of activity. However, especially as the Haynesville and Appalachia face pipeline constraints and bottlenecks, there is an opportunity for Barnett producers to capitalize in the current price environment by refracing wells. In July, Barnett operator BKV announced that it had completed over 200 refracs in the Barnett Shale in 2021. While refracs are difficult to generalize, BKV has indicated that refracs allow the company to maintain flat production with “even slight growth”. As Barnett operators continue to explore refracing wells, this could impact the overall declining rate of production in the region, and due to its geographic proximity and existing infrastructure, some Barnett producers are positioned to capitalize on today’s strong gas prices. For a more in-depth dive into Barnett economics and refracs, contact BTU for a sample of our Upstream Outlook.