Following the UN Climate Change Conference (COP26) in Glasgow last month, the Biden Administration announced the formation of a new Energy Division within the Office of Science and Technology dedicated to the pursuit of national climate goals including the President’s previous commitment to a carbon-free electricity system by 2035. While renewables development continues to accelerate across much of the country, intermittent generation, inadequate energy storage, and inter-regional transmission constraints suggest an ongoing need for dispatchable generation in the intermediate term. As unfavorable economics continue to push coal plants into retirement, it appears gas plants are likely to fill this role, but despite having a lower carbon emissions intensity, these plants may remain a significant obstacle to full grid decarbonization by 2035. If natural gas is to remain a part of the US power supply stack, the widespread deployment of carbon capture and storage (CCS) may be required to sequester plant emissions. Today’s Energy Market Insight will explore a scenario where widespread CCS is implemented on the US natural gas fleet to achieve grid decarbonization.

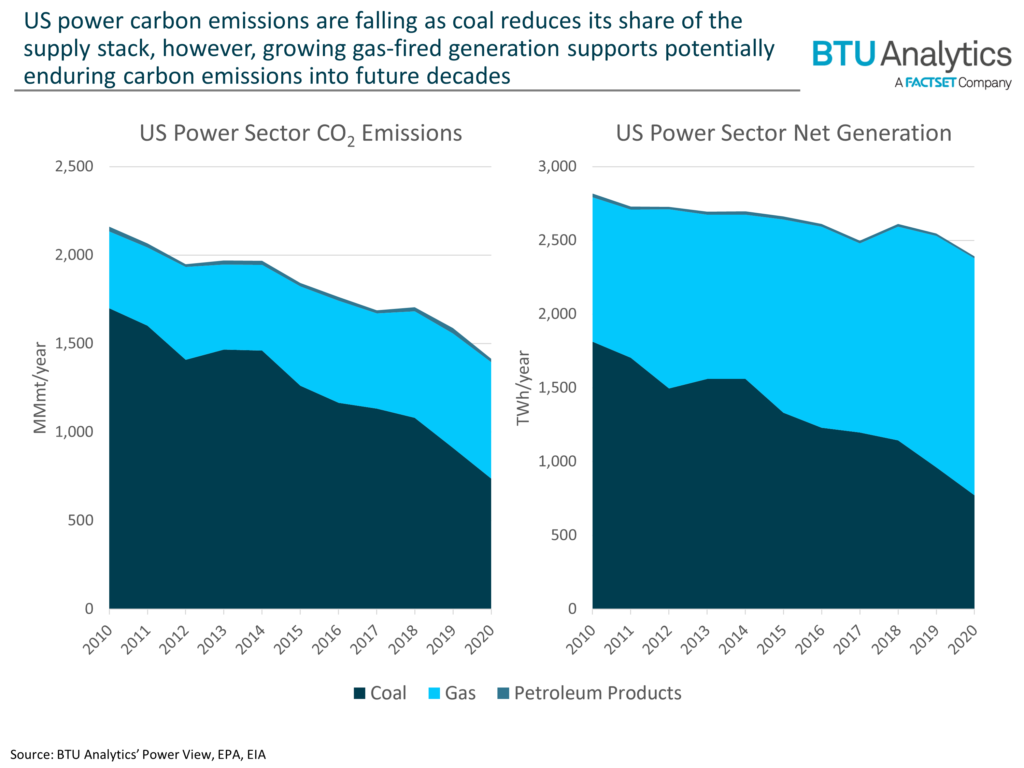

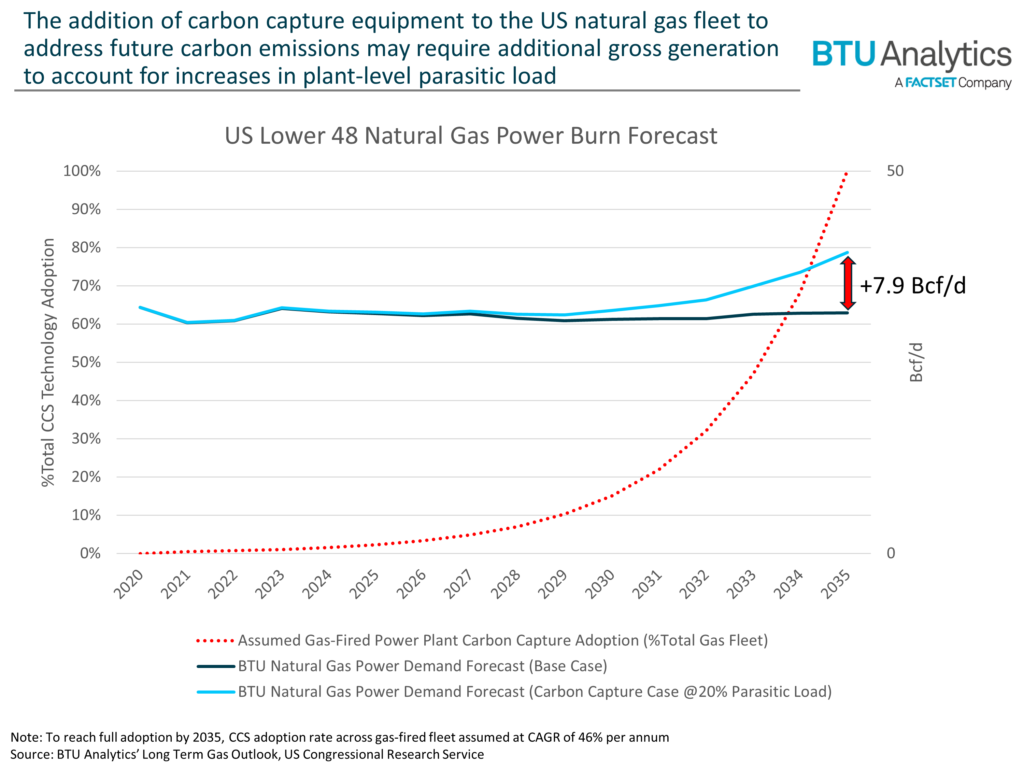

The share of US fossil-fueled generation provided by coal shrank by 58% over the last decade, from 1,813 TWh in 2010 to 772 TWh in 2020. As natural gas grew to become a dominant part of the fossil generation stack, overall power sector emissions fell by 35%. Despite this promising initial reduction in emissions, limits to future coal displacement and growth of the gas fleet restrict future possible emissions reductions. Let’s assume that to reach President Biden’s 2035 decarbonization goal, regardless of economic and engineering obstacles, widespread CCS is rolled out on the US gas fleet. How would that impact natural gas power generation and natural gas demand? According to a recent report by the US Congressional Research Service, the energy costs associated with capturing and compressing CO2 from a plant’s exhaust stream represent approximately 20% of a power plant’s generating capacity. When deploying CCS at scale, this reduction in plant efficiency may create a sizable increase in the required generation (and corresponding natural gas demand) from the same gas plants required to serve demand on the grid.

Ironically, full decarbonization of the gas fleet would require increased investment in natural gas infrastructure to fill the generation shortfall associated with deploying CCS. Not only would increased power generation require a corresponding increase in gas production, but it could also require additional pipeline buildout or capacity increases, particularly in regions with limited local production. According to BTU Analytics’ base forecast from the Long Term Gas Outlook, US Lower 48 natural gas power demand is forecasted to average 31.5 Bcf/d in 2035, up from 30.2 Bcf/d in 2021. This forecast already assumes aggressive growth in renewables with wind and solar capacity more than tripling between now and 2035. Assuming 100% CCS adoption by 2035, power demand could increase up to 7.9 Bcf/d due to incremental parasitic load. If all incremental demand were to be met by US gas production, it would result in more than a 7% production increase relative to BTU Analytics’ current base forecast. For US regions without local production, this increase in gas demand will likely also require additional gas pipelines to import new supply.

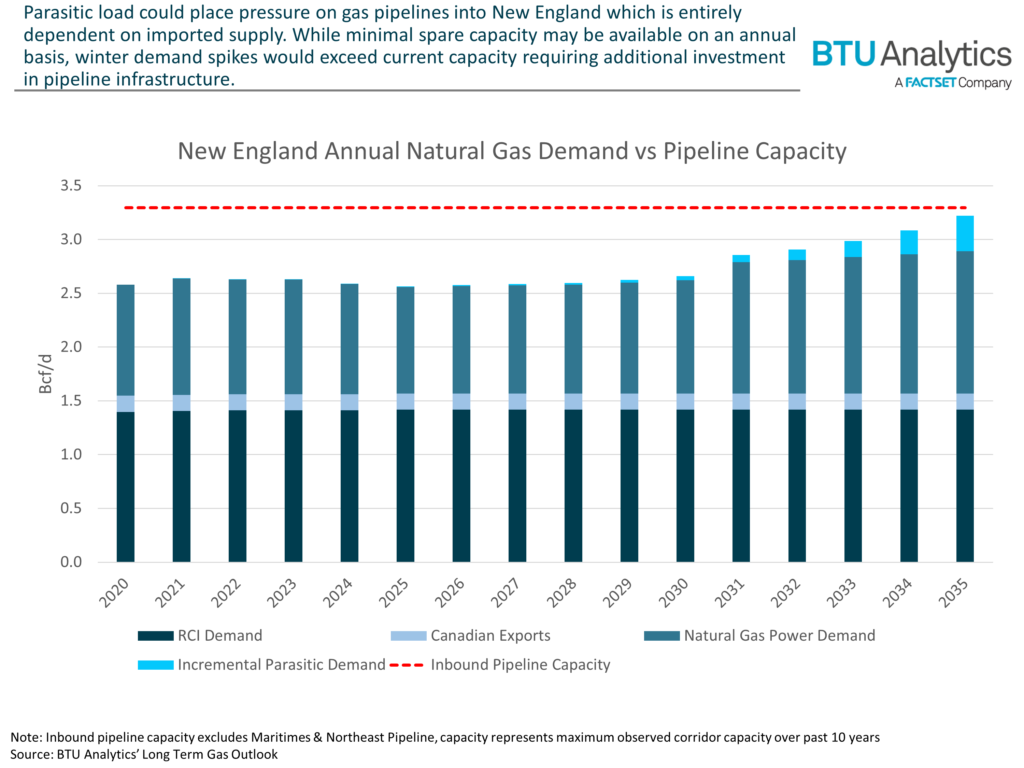

One region that may see infrastructure constraints in such a scenario is New England. While the political climate in New England is not currently favorable to increased investment in fossil fuels, full decarbonization of the natural gas fleet would put stress on existing pipeline infrastructure. BTU Analytics’ forecast estimates an incremental 330 MMcf/d of power demand would be added to the region due to parasitic load. Currently, utilization of pipelines into New England from Appalachia and Canada is averaging 88% on an annual basis. However, utilization ticks up to 94% during the winter when demand for natural gas heating is strongest in cities like Boston. Using the maximum observed corridor capacity over the past 10 years, New England has just over 200 MMcf/d of open capacity during the winter months and approximately 400 MMcf/d of capacity annually.

While individual US regions, such as New England, may not see material demand growth relative to overall US demand, regional constraints may still lead to unintended consequences as the US pursues full decarbonization of the natural gas fleet. In addition, the interplay between power markets, emissions solutions, and the natural gas market will become increasingly important as climate goals become more ambitious. BTU Analytics provides insights on these markets through our suite of products including the Power View, the Henry Hub Outlook, and the Long Term Gas Outlook. Request a sample of our reports today by contacting us at info@btuanalytics.com.