Once touted for their prime location and economic potential, Oklahoma’s SCOOP and STACK plays saw rapid increases in investment in 2017 and 2018. However, high drilling and completion costs and inconsistent well results due to complex geology yielded questionable economics for many operators. Rapid declines in SCOOP and STACK activity ensued as commodity prices dipped in recent years, which led diversified operators to consolidate capital investment in basins with stronger economics. Today’s Energy Market Insight will examine economic viability of Oklahoma’s SCOOP and STACK plays, particularly given recent strength in natural gas prices.

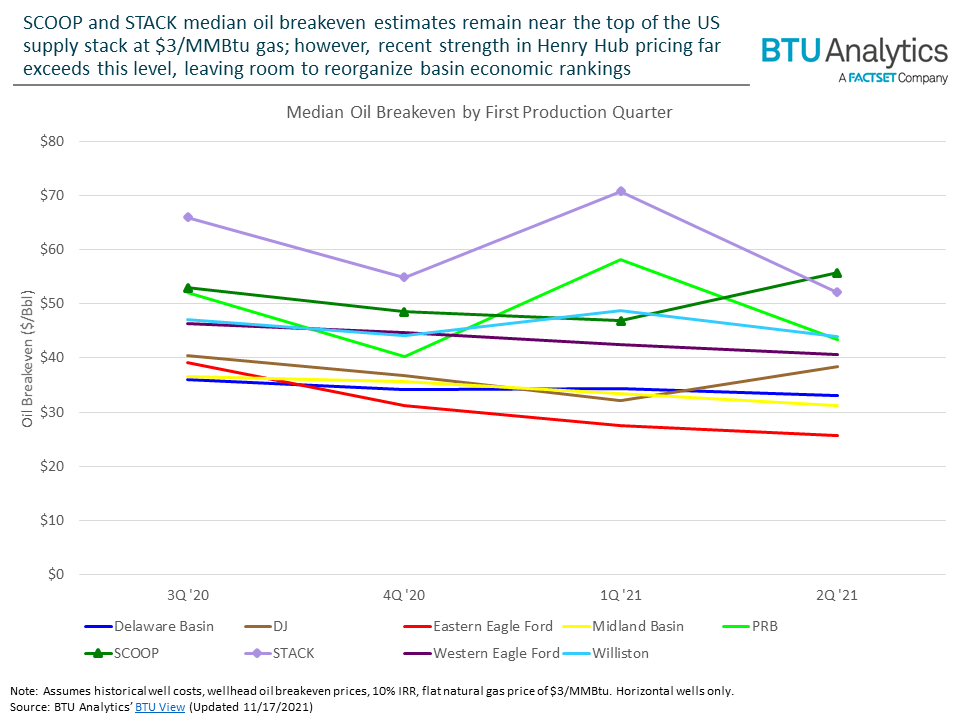

Like many other basins, Oklahoma’s 2020 horizontal rig count plummeted by over 80% from January to July. In keeping with the capital discipline mantra and free cash flow generation focus of the Shale 3.0 era, the late 2020-2021 recovery in drilling activity in Oklahoma has been slow relative to the Permian Basin and other economically advantageous regions. The chart below highlights that recent SCOOP and STACK wells continue to breakeven at higher oil prices than most other basins at a $3/MMBtu natural gas price assumption.

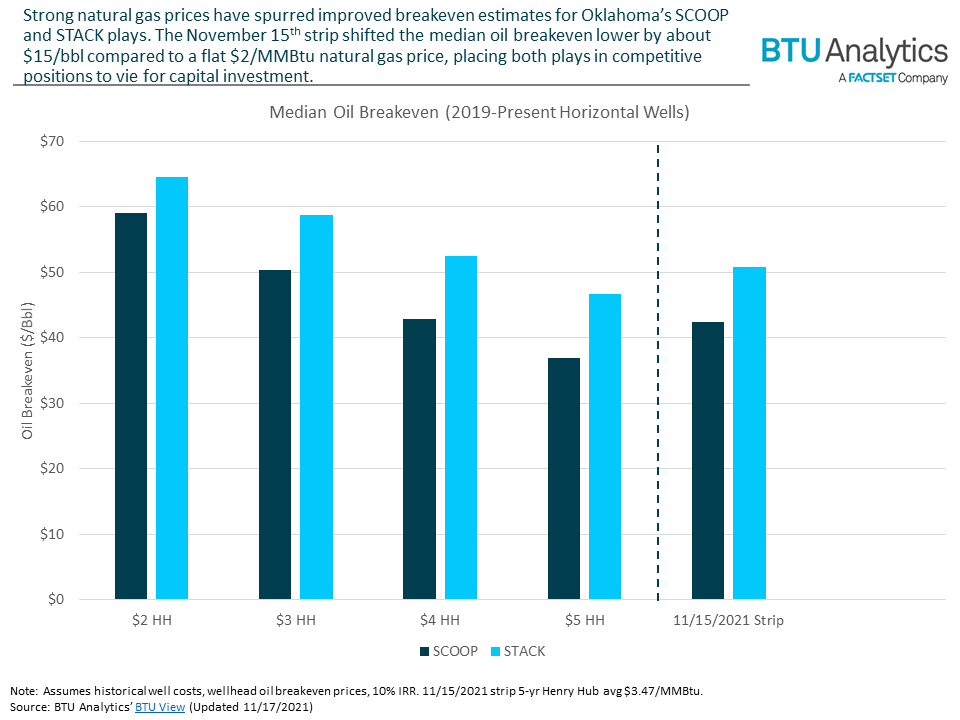

However, current Henry Hub prices far exceed $3/MMBtu, which casts a much more flattering glow upon Oklahoma’s shale play economics. Rife with associated gas, pockets of Oklahoma acreage offer significantly better economic results at higher natural gas prices. The November 15th Henry Hub strip price averaged $3.47/MMBtu over the five-year window when the majority of associated gas production from recent wells would occur. The chart below demonstrates the sensitivity of SCOOP and STACK economics at various natural gas prices.

Recent SCOOP well economics continue to outperform their STACK counterparts, and this remains true when incorporating the impact of higher natural gas prices. The latest monthly update to BTU’s economics dataset positions the median breakeven for both SCOOP and STACK 2019-present horizontal wells below that of the flat $4 Henry Hub price deck due to stronger near-term gas prices. With $40-$50/Bbl typical oil breakeven prices at the recent gas strip, Oklahoma’s SCOOP and STACK present a viable case for strong cash flow generation, a stark departure from the $60-$70/Bbl levels needed at $2 natural gas price levels commonly observed in recent years.

Improvements in natural gas prices have provided much-needed uplift for Oklahoma’s SCOOP and STACK oil economics, pushing them into profitable territory to contend for E&P companies’ capital investment as 2022 budgets are announced in the coming months. For more information about economics at the well, operator, and basin-levels and remaining inventory runway, contact us to set up a demo of BTU Analytics’ BTU View platform. With monthly updates capturing new wells and additional production history, the economics data set continues to provide up-to-date snapshots using the latest available state production data.