In recent weeks, we have seen two former giants of the Rockies natural gas plays, Encana (NYSE: ECA) and WPX Energy (NYSE: WPX), take different strategies to reduce their current and future exposure to demand payments on natural gas pipelines. In May, Tallgrass revealed that it had negotiated a new contract with Encana. The new contract reduced demand payments in the short term but resulted in a longer tenor contract, resulting in an increase in total revenue to Tallgrass. Subsequently, WPX Energy announced on May 25 that it entered into an arrangement with Citadel NGPE, LLC (Citadel) to pay Citadel $239MM to buy its future obligations on four regional Rockies pipelines. The obligations have future capacity demand payments of nearly $400MM.

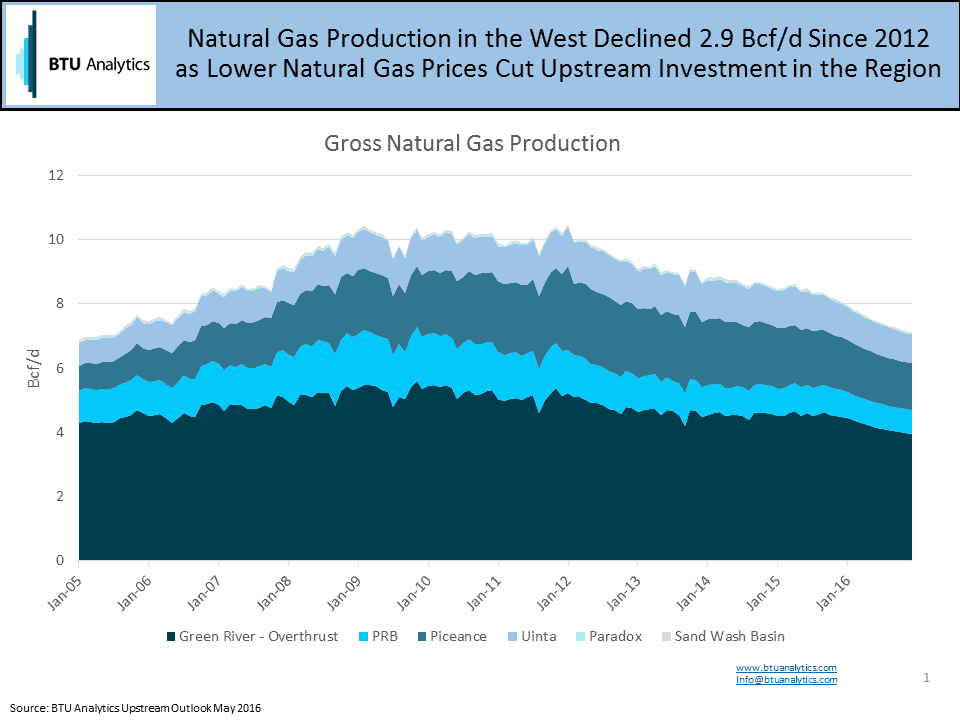

In both cases, the pipeline commitments have been primarily on pipelines serving the Piceance and Green River basins in the Rockies. Investment in developing Rockies natural gas supply has continued to fall since the pipeline construction boom of 2005-2011 when the Rockies added 3.7 Bcf/d of greenfield natural gas pipeline capacity (REX, Ruby and Bison). BTU Analytics estimates in our Upstream Outlook that natural gas supply from the Piceance, Uinta, Green River and Powder River Basin has declined a combined 2.9 Bcf/d from 2012 through May 2016 and Rockies natural gas declines will continue until natural gas prices recover enough to spur additional investment.

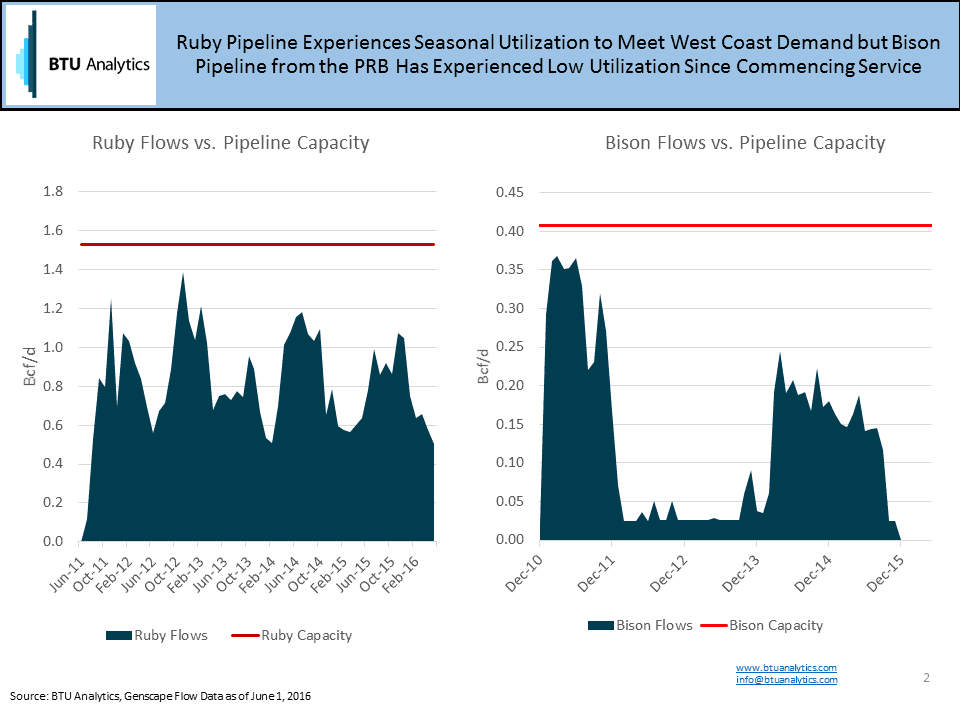

The impact of declining production has been the under-utilization of the newer greenfield pipelines as well as the existing pipelines in the region (Northwest Pipeline, TransColorado, CIG, Trailblazer, Cheyenne Plains, etc.). The chart below highlights the historical flows versus pipeline capacity for Ruby Pipeline, owned by Kinder Morgan and Veresen, and the Bison pipeline owned by TransCanada.

Ruby Pipeline transports gas from the Opal Hub in Wyoming to Malin, California where it then competes with Canadian supply sourced via GTN pipeline for market share in California. Seasonally, Ruby Pipeline has been able to maintain higher utilization rates with peak monthly flows reaching about 1.2 Bcf/d in 2014 and base-load volumes of about 0.6 Bcf/d. However, the base-load throughput is still well below its total 1.5 Bcf/d of capacity into the West Coast market. Bison pipeline was developed to support Powder River Basin coalbed methane production and transports gas from eastern Wyoming north into Northern Border Pipeline. When the pipeline first opened, shippers ramped up volumes to nearly fill the pipeline, but changing natural gas pricing spreads and declines in Powder River volumes left the pipeline empty until the polar vortex of 2013. As storage volumes in the Canadian and Midwest markets have replenished, Bison flows have since returned to zero.

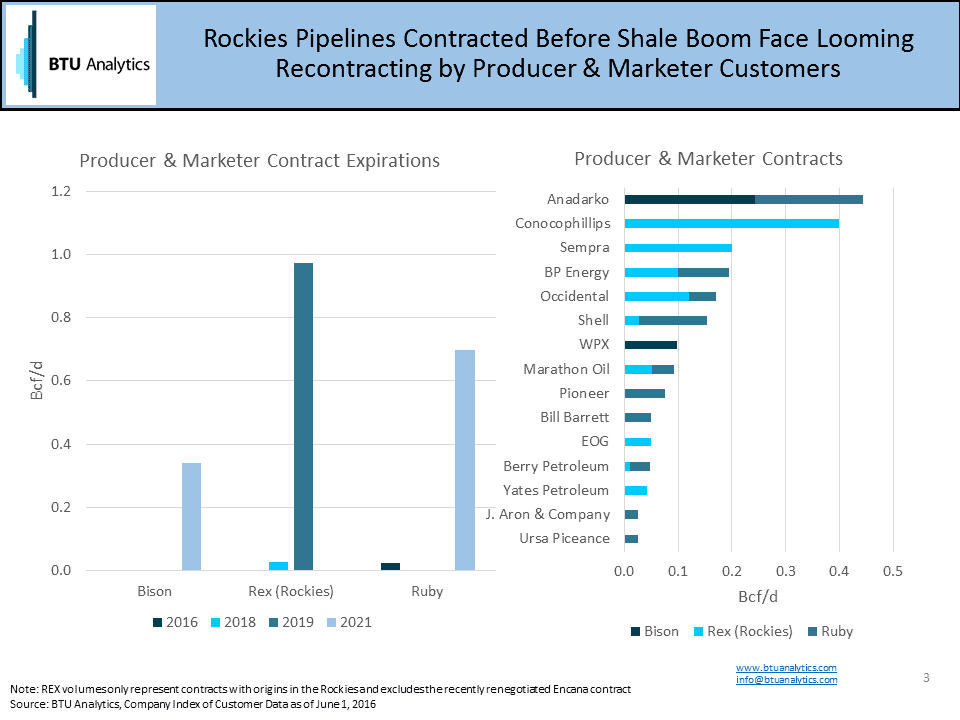

With supply declining and excess capacity available out of the Western Rockies, it’s no surprise cash strapped producers are looking for ways to reduce their exposure to future demand payments on these pipelines. The above graphic highlights for REX (Rockies origin contracts only), Ruby, and Bison the remaining long term producer and marketer contracts with expiration dates before 2021. While REX Pipeline has managed to negotiate a contract with Encana it’s to hard to imagine all three pipelines will be able to maintain all of these contracts as the majority of these producers have all shifted capital budgets away from natural gas and away from the Rockies to focus on the Permian and Eagle Ford.

On a monthly basis, BTU Analytics publishes their forecast for 90 producing sub-regions across the US and Canada taking into account infrastructure, producers sentiment, well level economics and many other factors to derive the most accurate and transparent forecasts in the industry. CLICK HERE to request a free copy and learn more about our services.