In the oil crash of 2015, producers communicated a strategy of high-grading to survive and maintain production despite lower prices. Roll the tape forward five years and the discussion of high-grading has returned, but this time not in the Bakken and Eagle Ford, the two largest plays at the time, but rather in the Permian basin. Today’s energy market commentary will explore the ability for producer’s to high grade Permian activity as oil prices recover and the potential impacts to Permian oil production.

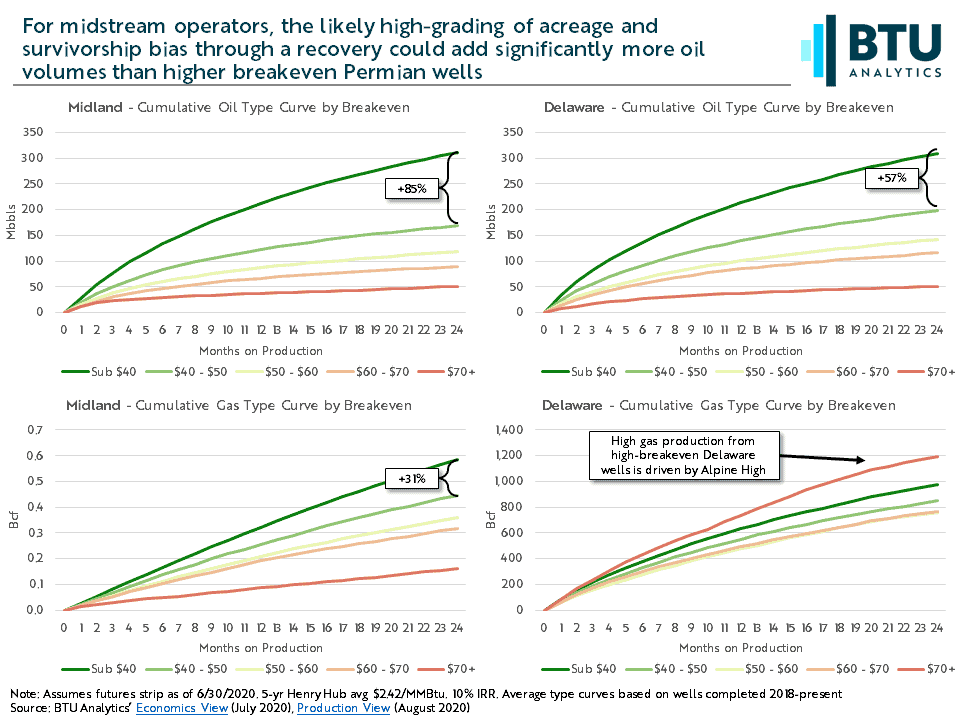

In late 2014 through 2016, producers openly communicated a strategy of targeting their best rock, while ignoring lower tier acreage and plays. A historical analysis of wells turned to sale in this time frame by breakeven distribution lends credence to this, particularly in the Bakken. Bakken producers, more so than other US oil shale plays, were forced to target the core and their best quality acreage resulting cumulative 24 month well productivity increasing by 39% from 2014 to 2017. Now, as the Permian has reached the later innings of delineation, high-grading and survivorship bias are likely to begin to take on a larger role, having a significant impact on overall production. The average well-productivity between top tier Sub $40/bbl breakeven wells is 85% and 57% larger on a cumulative 24-month oil production basis than even the next tier of $40-$50 breakeven wells for the Midland and Delaware, respectively. This can be seen in the chart below, which shows cumulative type curves for oil and gross gas production for Midland and Delaware Basin wells completed from 2018-present.

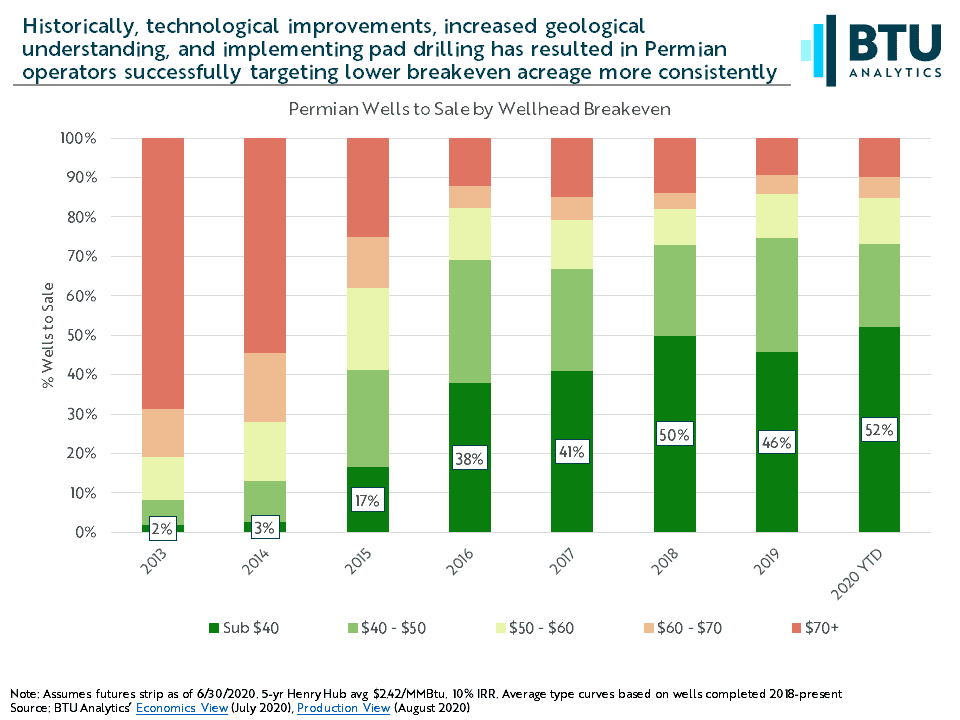

Using BTU Analytics’ Economics View analysis tool, shows a sample of 1,047 horizontal wells turned to sale in the Permian YTD in 2020, 52% had a breakeven in the top tier, Sub $40/bbl category, compared to 46% in 2019 and 50% in 2018.

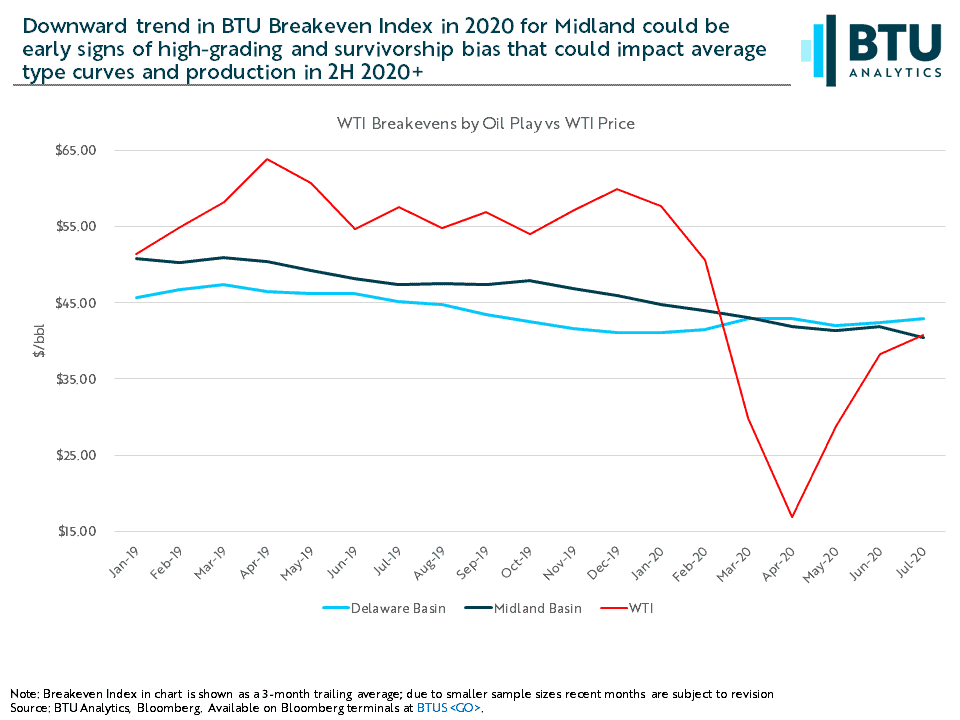

Pairing these trends with our leading indicator BTU Index, which plots spuds against micro breakeven grids developed as part of the Economics View tool, there are early signs that the wells that could come to market over the next 12 months may be more heavily weighted toward the more productive, lower breakeven wells, especially in the Midland Basin.

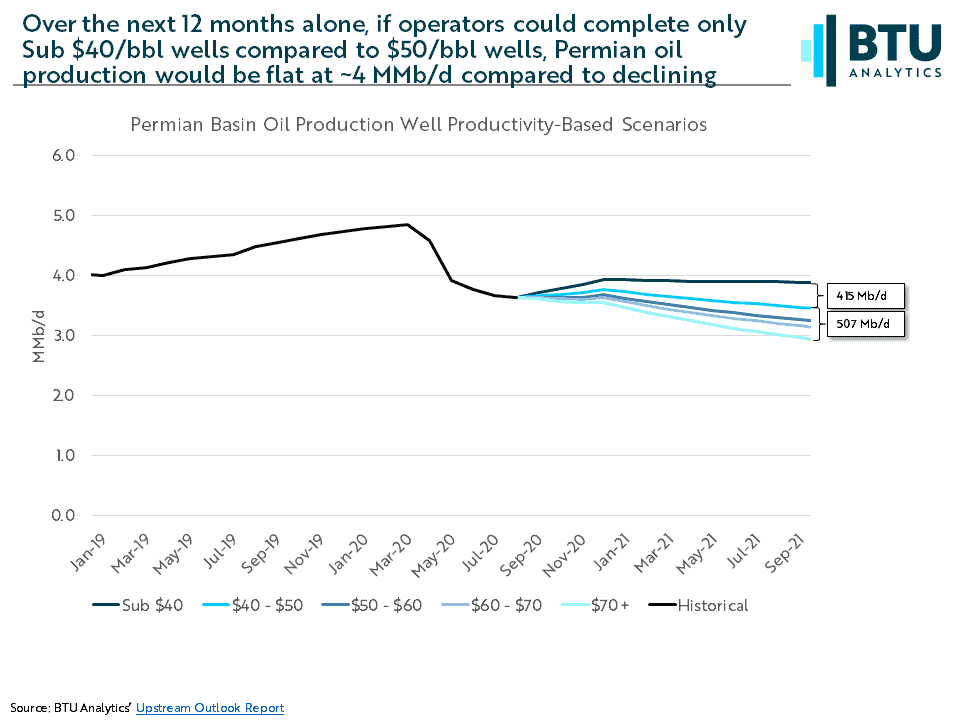

Translating the potential impact of high-grading and survivorship bias to oil production forecasts in the Permian shows a range of outcomes. To examine the potential magnitude of impacts, we used a simplifying assumption of a flat horizontal Permian rig counts of 124 in perpetuity and excluded Permian DUCs from this analysis. This allows us to isolate the impact of well productivity on production trends. There is almost a 1 MMb/d difference between a production outlook based on average well productivity that mirrors $70+ breakeven productivity compared to Sub $40 wells highlighted in the first chart.

Furthermore, of the 1 MMb/d delta, 415 Mb/d of it is driven by the difference in productivity of a top tier Sub $40 breakeven wells compared to a second tier $40-$50 breakeven well and is also the difference between a flat versus declining production profile over the next 12 months.

Well productivity trends, DUCs, curtailment roll backs, and cash flow will all work in combination to dictate the road to recovery in not only the Permian Basin, but other shale plays as well. A deep understanding of how these drivers impact the production outlook can be used to identify future business opportunities and drive strategy. For more detailed well-level and operator analysis relevant to your business, request a demo of the Economics View and Production View tools from BTU Analytics.