The collapse of crude prices in 2020 spurred a rapid decline in oil & gas drilling and completion activity as E&P companies tried to cut spending until market conditions improved. BTU Analytics noted that service companies were caught in the crossfire last year, driving service costs to rock-bottom prices. Now that commodity prices have improved, well costs are on the rise as service companies regain negotiating power with fewer sidelined drilling rigs, completion spreads, and other ancillary equipment and crews. Additionally, the cost of key materials, such as steel and fuel, have inflated from 2020 levels. Today’s energy market insight will examine the causes of well cost inflation, what E&P companies are doing to combat them, and the outlook for well costs for the remainder of 2021 and beyond.

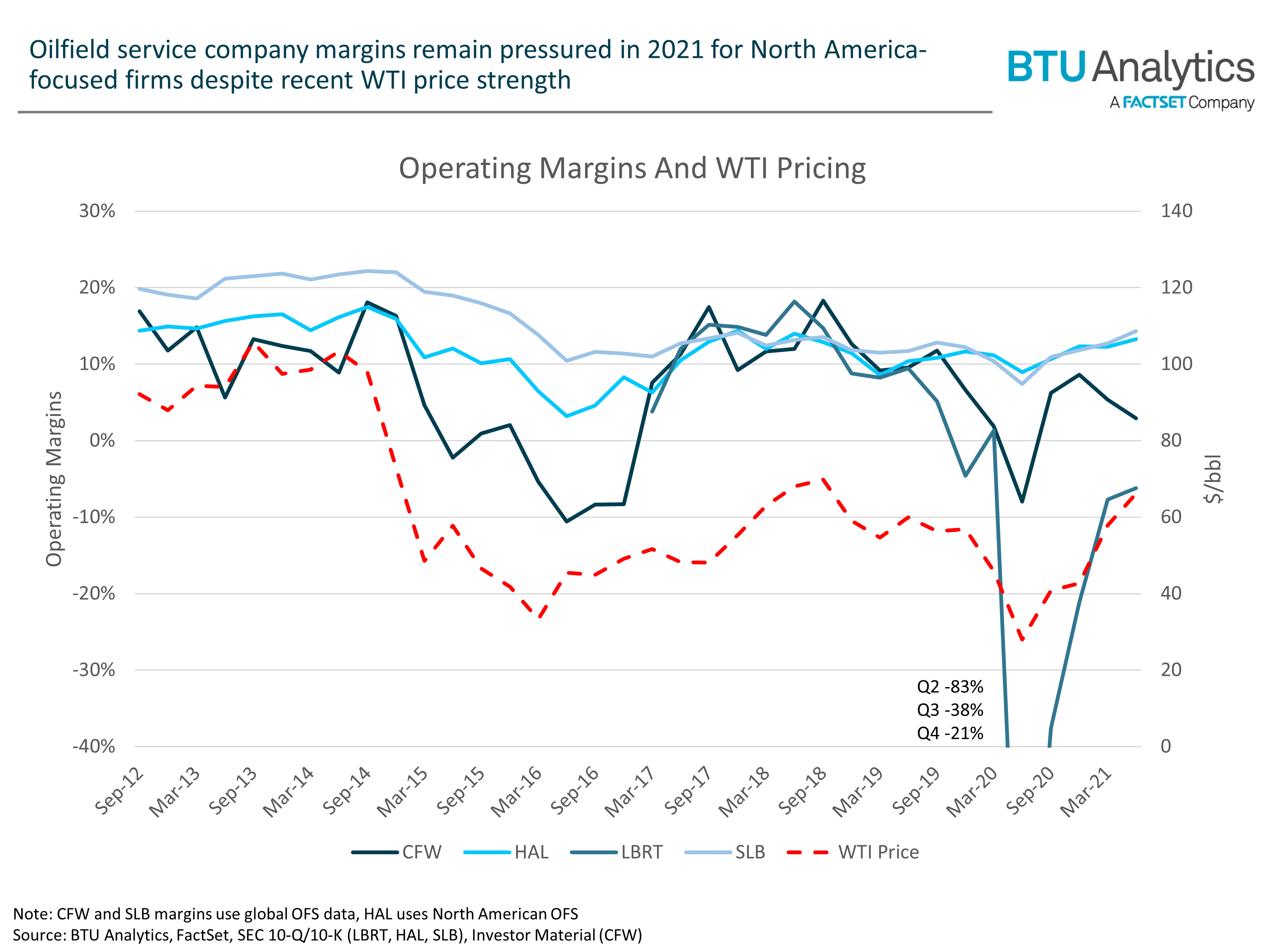

Oilfield service company margins were severely impacted in 2020 due to the rapid decline in drilling and completion activity when WTI prices plummeted. Halliburton and Schlumberger, the most international and diversified heavyweights of the group, were able to maintain margin integrity throughout the pandemic far better than drilling and completion-centric peers. BJ Services and Calfrac Well Services, two notable fracturing competitors, filed for bankruptcy protection in July 2020. Shortly after, Liberty Oilfield Services (NYSE: LBRT) doubled down in the completions space by acquiring Schlumberger’s OneStim onshore US and Canadian fracturing business unit, but Liberty’s operating margins still remain tight in 2021 despite strong WTI prices. Tight margins for most service companies will continue to pressure well cost increases throughout the year, forcing producers to get creative to sustain recent drilling, completion, and equipment (D,C&E) efficiencies baked into 2021 capital budget assumptions.

Several publicly traded E&P companies acknowledged the changing price environment for oilfield services in their recent earnings materials. Between the uptick in drilling and completion activity, supply chain bottlenecks driving higher material costs, and increased service company negotiating leverage, well costs are poised to rise in 2021 barring substantial new operational efficiencies. The Permian Basin, which dictated the rate of shale activity recovery in 2020, is home to a multitude of responses to well cost inflation pressure. Diamondback’s Midland Basin 2021 D,C&E guidance was $520-580/lateral ft in June investor materials, up from an average of $538/ft in 2020 actual well costs, acknowledging that well cost increases would be necessary later in the year as service companies’ financial health improved. However, in last week’s earnings announcement, Diamondback lowered Midland Basin 2021 D,C&E guidance to $520-550/ft, essentially targeting flat well costs for the remainder of the year. The decision to stop calling for increased well costs this year appears to have resulted from faster drill times, broader simulfrac applications, and fewer planned rigs and completion crews.

Another strategy for managing well costs is to lock in the price of supplies needed for upcoming D,C&E projects. Several companies, particularly in the Permian Basin, have turned to using local sand instead of premium white sand mined in the Midwest. Laredo Petroleum (NYSE: LPI) recently cited savings of about $200,000 per well by utilizing sand mined in Howard County, TX for completions in the same county, which shielded the company from rising sand costs from third-party sources in recent months.

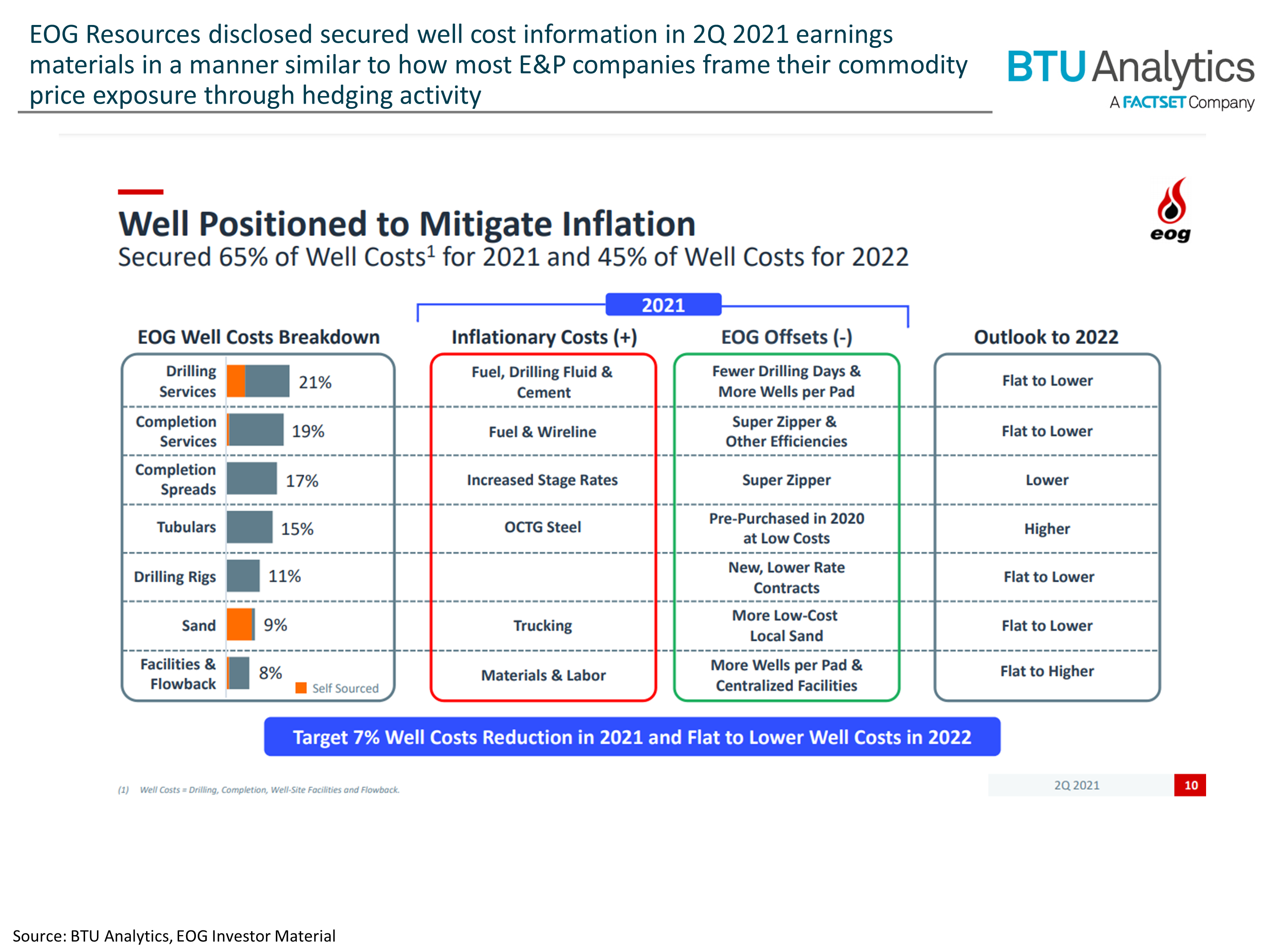

Perhaps the most interesting strategy to offset rising well costs was disclosed by EOG in 2Q21 earnings materials. EOG aims to not only utilize further operational efficiencies to maintain costs. They locked in future well costs by pre-purchasing steel in 2020. By pre-purchasing goods when prices were low last year, E&P companies could effectively hedge a portion of their future well costs. EOG’s offsetting measures claim to have secured 65% of well costs in 2021 and 45% in 2022, providing clear goal posts for near-term AFE budgeting. Most producers were cutting capital investment in 2020, but the few that had the foresight to secure supplies while commodity prices were low will have greater flexibility in 2021 and 2022. This strategy is primarily feasible for E&P companies of scale, leaving less active firms subject to the current rate for services and necessary supplies.

Service company margins have improved from the troughs reached in 2020, but the first half of 2021 did not provide substantial relief to many drilling and completion-focused service companies. Strength in steel and fuel prices has recently added pressure to E&P companies’ capital budgets, pressuring them to target faster operations and find new efficiencies to sustain recent well cost improvements. The divergence between E&P companies of substantial scale and smaller firms with greater exposure to market conditions will likely become prominent in the second half of 2021, potentially leading to upward revisions in capital spending to meet guided levels of drilling and completion activity. To get BTU’s take on how this will impact projected activity levels, consider subscribing to our Upstream Outlook service. For context of how trends in well costs impact breakeven economics, request information about our Oil & Gas Economics View product.