Last June, BTU Analytics examined the outlook of horizontal drilling in the Uinta Basin. As oil prices recovered, total annual drilling activity increased in the Uinta Basin. As drilling increased, producers shifted towards horizontal activity rather than vertical. Despite initial production rates exceeding 1,000 BOE/d, the basin’s viability remains challenged. First, the high paraffin content of Uinta oil contributes to higher transportation and refining costs. As a result, producers receive steep discounts for the waxy crude. Second, BTU Analytics estimates breakevens for the wells are marginal in today’s $60 WTI environment. With producers focused on trimming capital budgets, marginal plays continue to see dwindling capital.

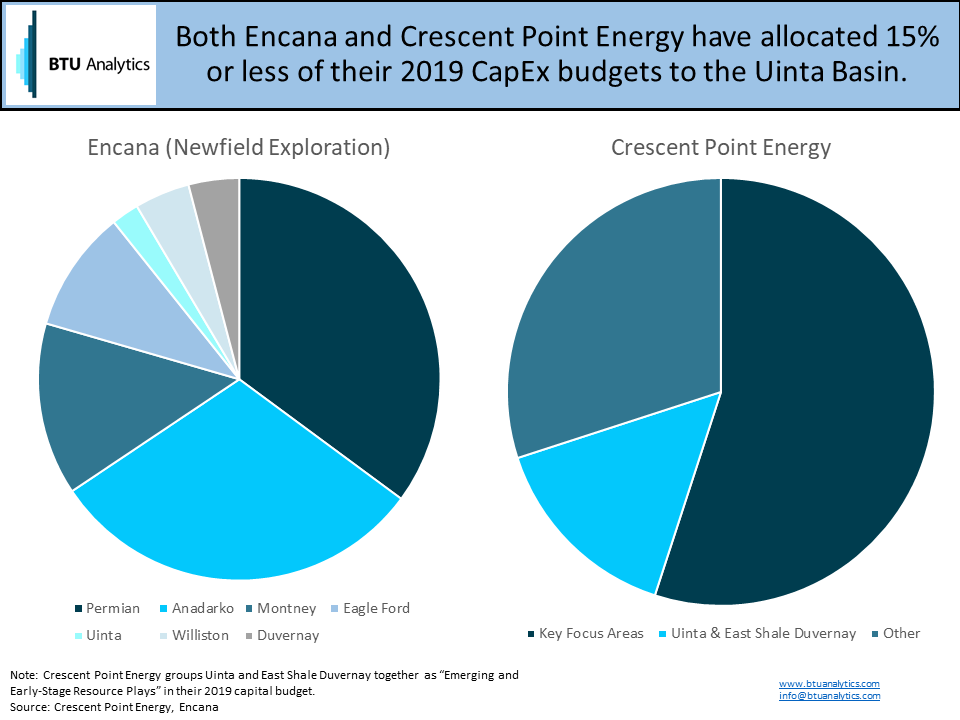

Encana, which acquired Newfield Exploration last month, and Crescent Point Energy combined for 62% of horizontal drilling in the Uinta during 2018. Despite their positions as leaders in Uinta horizontal drilling, neither operator currently prioritizes investment in Utah. The chart below shows 2019 CapEx budgets for the top two drillers.

Encana listed the Permian, Anadarko, and Montney plays as its core assets. Thus, a majority of its $2.7-2.9 billion capital budget for 2019 will be directed to these plays. Among its four “other” regions, the Uinta Basin will see the least investment this year of just $50-70 million. Similarly, Crescent Point Energy failed to designate the Uinta Basin or East Shale Duvernay as focus areas for 2019. In 2018, Crescent Point allocated 25% of its capital budget to the two plays. However, in 2019, the two plays will split 15% of Crescent Point’s $1.25 billion capital budget. Between all basins, Crescent Point and Encana will spend 30% and 20% less in 2019 than 2018. The producers are keeping in-line with the basin-transcending trend of reducing capital expenditures in 2019.

Another active operator in the Uinta Basin, EP Energy, recently started drilling horizontal wells after years of focusing on vertical activity. However, EP Energy’s investment in the basin will also be challenged in 2019. EP Energy recently disclosed concerns regarding liquidity in their 2018 10-K. These recent announcements beg the question- what are the breakeven economics for new wells in the Uinta Basin?

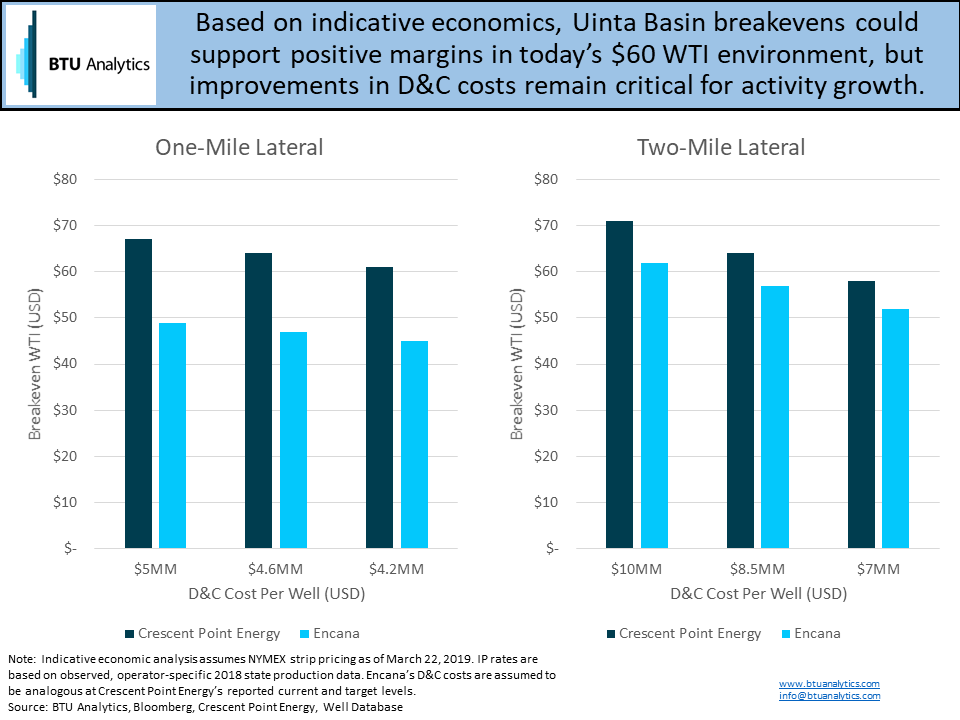

BTU Analytics’ reviewed the well results for the two most active horizontal drillers in the Uinta Basin to develop indicative well economics.

In 2017 and 2018, Crescent Point Energy’s drilling and completion (D&C) costs were $5 million for one mile lateral wells. Additionally, Crescent Point indicated 2 mile laterals cost between $8.5 and $10.0 million. From the same investor presentations, Crescent Point Energy’s planned development phase wells were aiming for targets of $4.2 million and $7-8.5 million. The decline represents an approximate 15% decrease in D&C costs per well. Encana has yet to disclose updated D&C cost estimates for the Uinta Basin. Due to a lack of disclosure on costs from Encana or prior by Newfield Exploration, BTU Analytics benchmarked well costs to Crescent Point’s D&C costs. While the wells now operated by Encana had higher production rates than Crescent Point’s, neither operator appears to be achieving high margins in the Uinta Basin compared to their key focus plays.

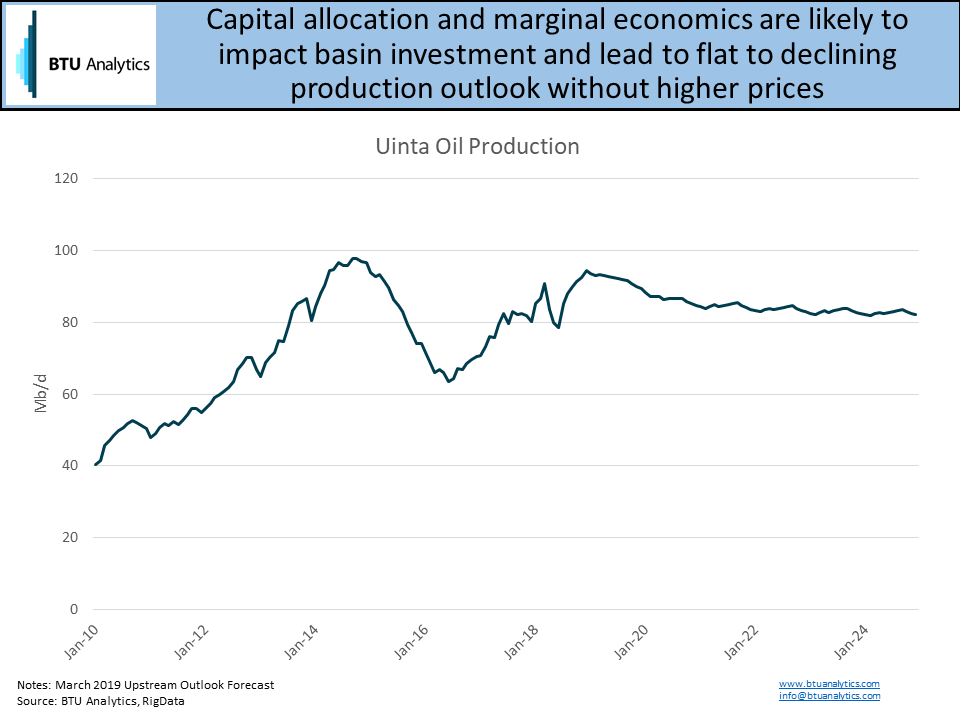

As a result, BTU Analytics expects activity in the region to fall from current levels and production to decline. As evidenced by this analysis’ indicative economics and operator budget declines, significant production growth would require stronger crude prices in conjunction with additional D&C efficiencies. Uinta Basin economics have improved in recent years, but will it be enough to secure future investment from a capital discipline-minded market? To learn more about BTU Analytics’ viewpoint on Uinta Basin production outlook, investigate our Upstream Outlook. For more thorough well-level economic analysis, request a sample of our E&P Positioning Report.