For years, fundamental analysts have forecast supply and demand by using historic trends to predict the future and ‘up and to the right’ was the name of the game. The power sector was a bright spot for demand forecasts as coal plants retired, new natural gas plants were built, and demand for power was assumed to increase at 1.5% – 2% a year, creating an opportunity for natural gas producers to expand activity to record levels. However, more recently, low load growth levels brings into question some of the assumptions many models once relied upon.

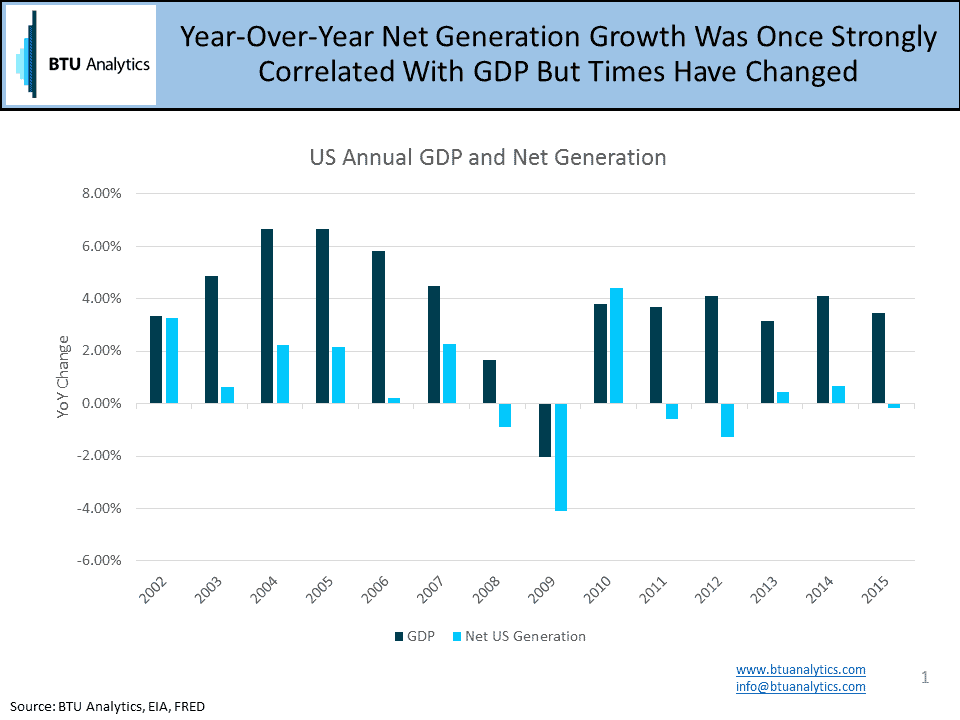

At one time, GDP was a reliable indicator of power demand growth. A growing economy meant more goods were being created and consumed and power was needed to drive that growth. But as the chart below highlights, this relationship no longer holds true. While annual GDP growth has been humming along at 3%-4% since the great recession, power demand growth has stagnated at around 0.2%. This story is not necessarily new, but it has the potential to impact demand in a meaningful way going forward.

A few theories exist as to why this phenomenon has become more pronounced in recent years. Lagging income gains for some Americans could impact both electricity usage and the continued acquisition of goods that consume power. Additionally, a rush over the last 30-40 years of consumers equipping their lives with electric goods has been more than offset by energy efficiency measures, more stringent building codes, and demand response systems limiting demand gains despite population growth.

As natural gas market analysts look forward, a lot of models predict continued growth from the power sector. But as renewables becoming a larger and larger slice of the generation stack, they are taking generation share from gas. The chart below shows the generation from wind and solar plants since 2010. BTU Analytics estimates that the demand erosion from this new segment now equates to at least 4 Bcf/d and has the potential to grow an additional 2 Bcf/d based on announced utility scale projects.

Finally, the heat rate of natural gas fired power plants has continued to decline over the past 10 years and now natural gas plants represent one of the more efficient generation sources. So while gas may be stealing market share from coal, the heat input required to produce the same amount of power is much lower than it once was. And with excess natural gas-fired capacity already in the power market, will the new gas-fired power plants just end up stealing market share from older, less efficient gas turbines?

The above highlights some dramatic hurdles that power burn faces over the next 5 years. With the threat of E&P activity cuts flipping the gas market to being potentially supply short over the next two years, some loss of power demand may not necessarily be a bad thing.