At the end of August 2018, the level of concern about the upcoming winter seemed muted as the December 2018 Henry Hub futures contract traded around $3 despite the fact that US gas storage levels were about 600 Bcf behind the 5-year average at the time. The consensus view could be summarized as new pipeline capacity was coming online in fall 2018 which would allow producers to grow supply to meet winter demand.

Fast forward to November 14, 2018, and new pipelines are online (Nexus and Atlantic Sunrise, for example) and production has grown (Appalachia pipeline production receipt flow samples have consistently sustained over 30 plus Bcf/d this week). But, like the flick of a switch as the winter gas market rips higher, we are in a demand driven winter gas market where the Henry Hub prompt futures is up over $1.30 this week to $4.80 per MMBtu today.

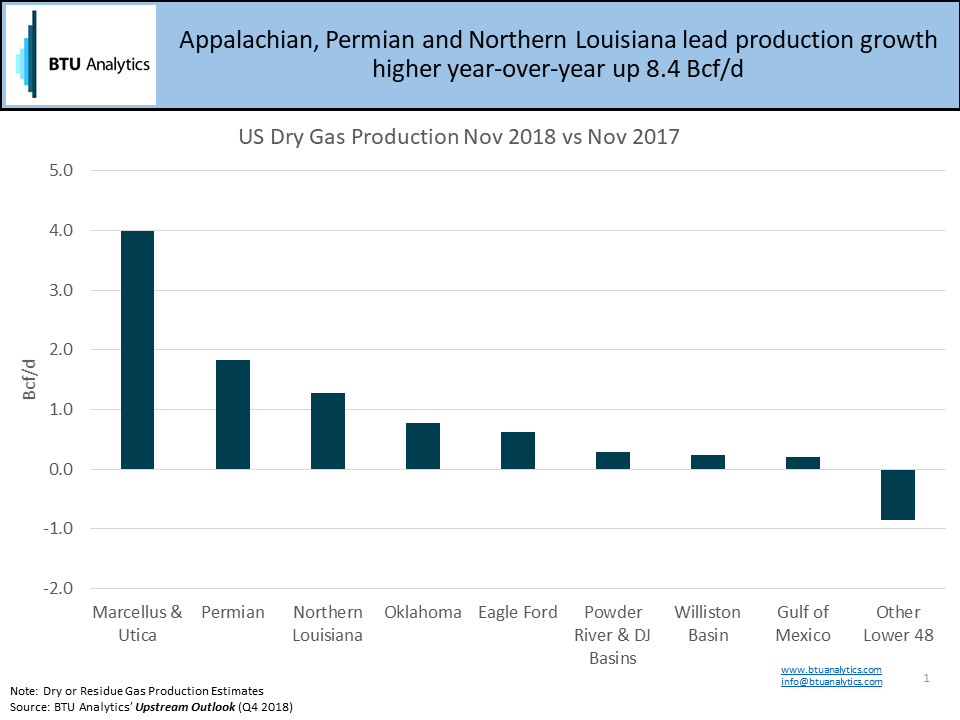

Gone is the summer 2018 gas market where pipeline constraints limited supply area growth, while supply area basis was weak and summer demand was met with futures not budging above $3 per MMBtu. In the current market, demand has grown faster than producers can respond with production gains. What has changed in the market going into winter 2018-2019? Supply, demand, and pipe capacity have all grown. As shown below, monthly modeled supply has grown across many supply basins year-over-year, with Appalachia leading the way at 4.0 Bcf/d thanks in part due to new pipe capacity. The challenge is demand has also structurally moved higher.

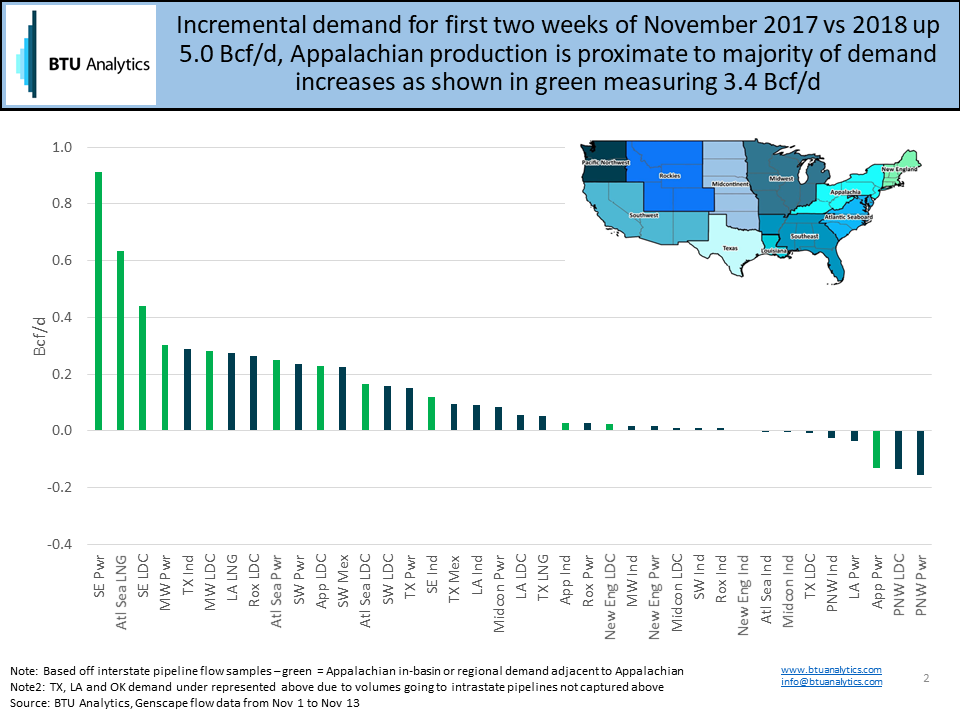

Looking at a demand sample (deliveries off of interstate pipelines) of regional demand by facility type, comparing November 2017 vs 2018, the 4.0 Bcf/d of Appalachian production growth is being soaked up by 3.4 Bcf/d of either Appalachian demand or adjacent regional demand to Appalachia, as shown in green below. The Southeast power, LDC and Atlantic Seaboard LNG (Cove Point) components represent the three largest year-over-year gains.

With Transco connecting Appalachia, the Atlantic Seaboard, and the Southeast, we can see below the impact on pipeline flows as winter demand has ramped up. Atlantic Sunrise started service October 6, 2018, and the increased volumes can be seen as flows south at the Virginia-North Carolina border approached 2 Bcf/d. As the recent ramp in demand has started (and note we are only talking about ‘November cold’ here) flows south on Transco have dropped by about 700 Mcf/d.

It seems the market finally cares about the 600 plus Bcf storage deficit to the five-year average and how much producers can ramp supply going into winter as the winter 2018-2019 strip is now priced over $4.50 per MMBtu, while the summer strip 2019 is below $2.80 per MMBtu. What does this mean as we roll into the peak winter months of January and February? How much inventory are producers carrying into winter? To access BTU Analytics’ view on Henry Hub and basis pricing, subscribe to the Northeast Gas Outlook service.