Followers of the energy markets have access to more data than ever. This week we were treated to a new data set from the EIA, estimates for crude oil production based on EIA-914 survey data. The new data from the EIA is a welcome addition in our eyes, but the amount of data being pushed to the market these days contributes to a great amount of noise that distracts from the more important changes and factors impacting this market.

Here are five of the most important factors to watch over the next six months:

- DUCs – We’ve written several pieces on the inventory of Drilled but Uncompleted wells and their anticipated impact on US production and both natural gas and oil prices. Ignore the potential market impact of these wells on prices at your own risk. (Previous Coverage Here: Can US Oil Production Really Fall?; Eagle Ford Completions Standoff; Producers Bagging DUCs, Bearish for Pricing)

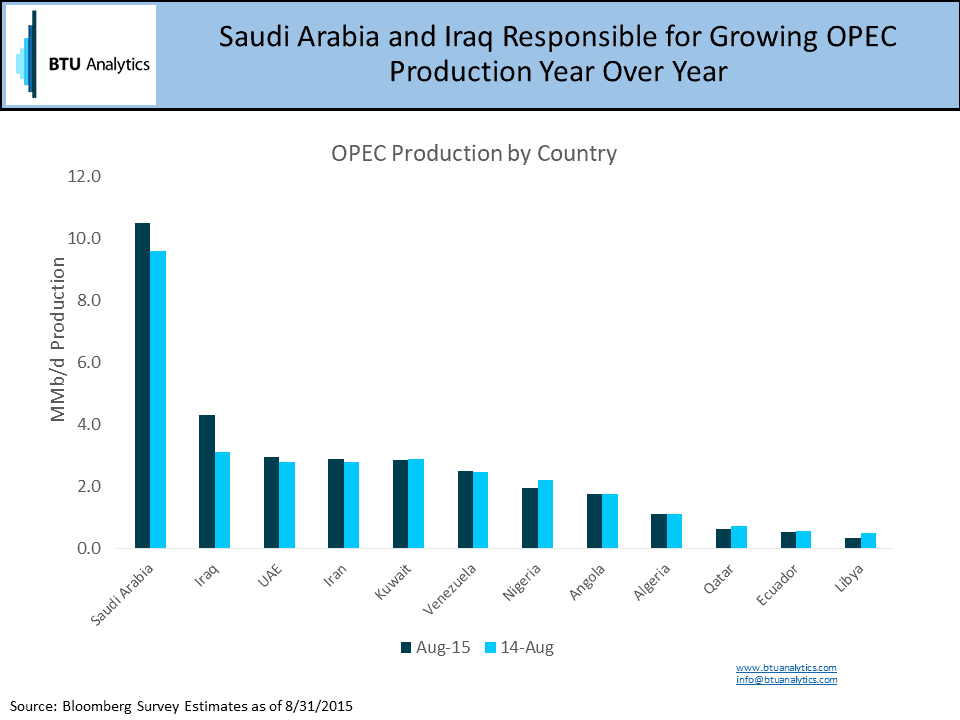

- OPEC Production Through Fall – OPEC production has grown to over 32 MMb/d this summer according to Bloomberg Survey estimates, driven by record output from Saudi Arabia and production increases in Iraq. We’ll be watching to see if Saudi maintains production at 10.5 MMb/d as domestic summer demand abates, or if the Kingdom keeps the pressure on, while Iran also waits in the wings looking to boost production following the lifting of sanctions.

- How Quickly Natural Gas Pipelines Fill This Winter – 2.1 Bcf/d of new pipeline takeaway is coming online in the Northeast later this year. The pace at which these pipelines fill this winter will give us an indication of whether Northeast producers will stick to long-term development plans or be responsive to market dynamics (Previous Coverage: Rex’s Slow Start, Northeast Gas Producers in ‘A Firm Dilemma’).

- Capital Inflows into North American Assets – US markets should find balance over time at these price levels, if only outside capital didn’t prop up companies that should go out of business and asset valuations that limit consolidation. (Previous Coverage Here: Will Outside Capital Continue to Prop Up Oil and Gas Activity?)

- Sabine Pass Commences US LNG Exports – Demand estimates for US LNG exports over the next five years vary wildly. One major point of contention is utilization of constructed capacity in the US. While this question won’t be put to rest in the next six months, witnessing the first exports from Sabine should provide some clarity to the market around how new facilities will ramp up and what previously unforeseen risks we might want to consider as the US enters the market as a major global LNG supplier. (Previous LNG Coverage Here: This Natural Gas Spread Too Shall Collapse?; Will Initial US LNG Exports Be Competitive?)

To follow these items and more, subscribe to BTU Analytics’ Energy Market Commentary here.