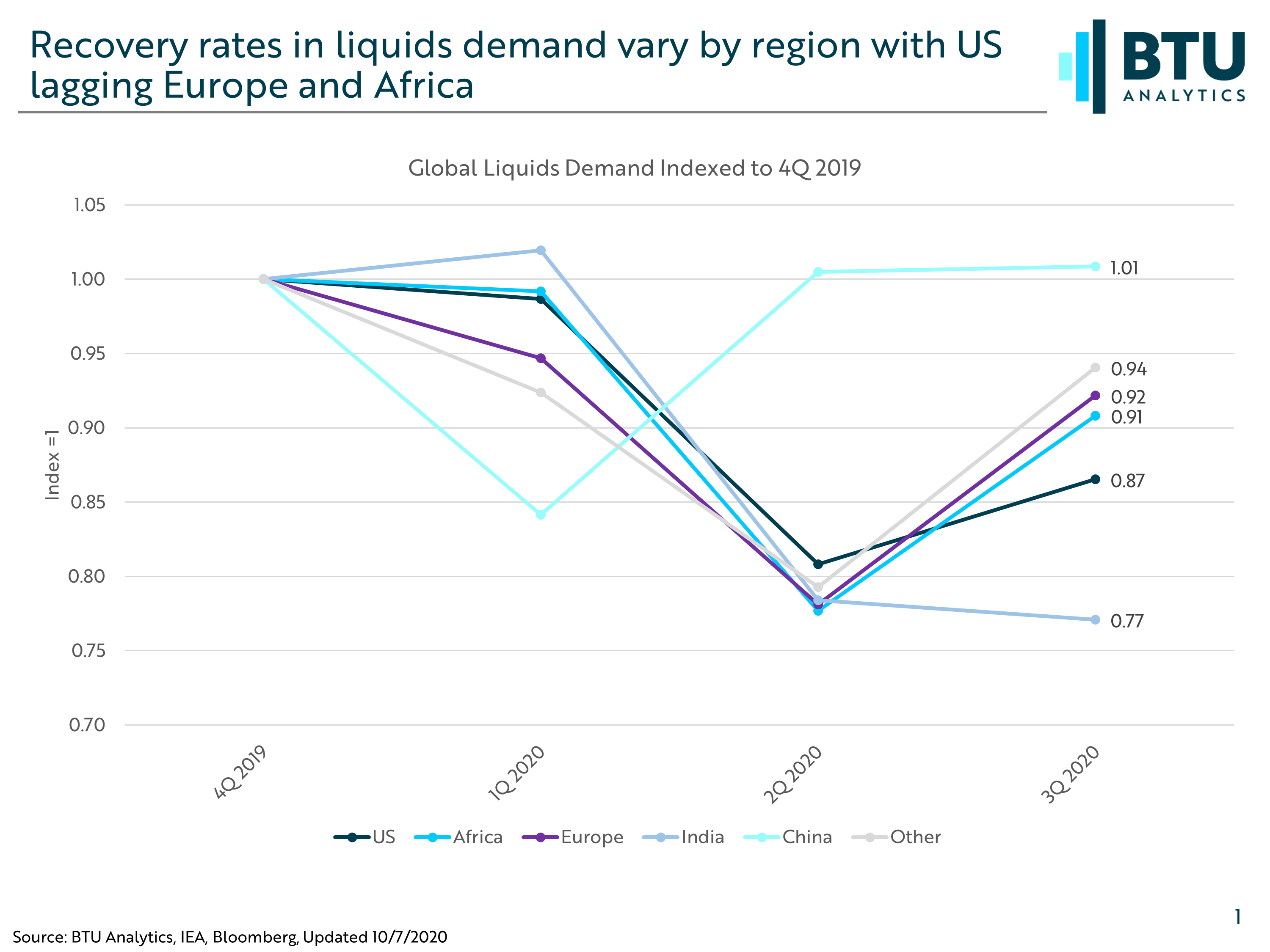

After reaching a trough in 2Q 2020, global oil demand has begun to rebound, and BTU and others model a steady recovery over the coming months and years. Preliminary 3Q demand estimates from IEA show that China has fully rebounded and that Europe and Africa have rebounded to over 90% of 4Q 2019 levels. The US is lagging these three regions and is at 87% of 4Q 2019 levels during the same time period. While a steady recovery is what is typically modeled ad assumed, the reality is that it could be lumpy and highly impacted by steps taken by different countries to control COVID 19, especially this winter.

After reversing an upward trend in cases early in the pandemic, European COVID cases have started to increase again this fall. While the general appetite to completely lockdown similar to earlier this year has waned significantly as pandemic fatigue and economic concerns continue to take their toll, governments continue to try to enforce varying degrees of lockdowns and restrictions. Some new restrictions may be less impactful to oil demand and come in the form of mandating masks outdoors as Italy recently implemented. Others like Belgium will mandate bars close at 11 pm instead of 1 am and reduce the number of close contacts a person can have down to three people from five. And still others like Spain have implemented regional travel restrictions. In Madrid, people are only allowed to travel outside their home districts for essential journeys in addition to bar curfews.

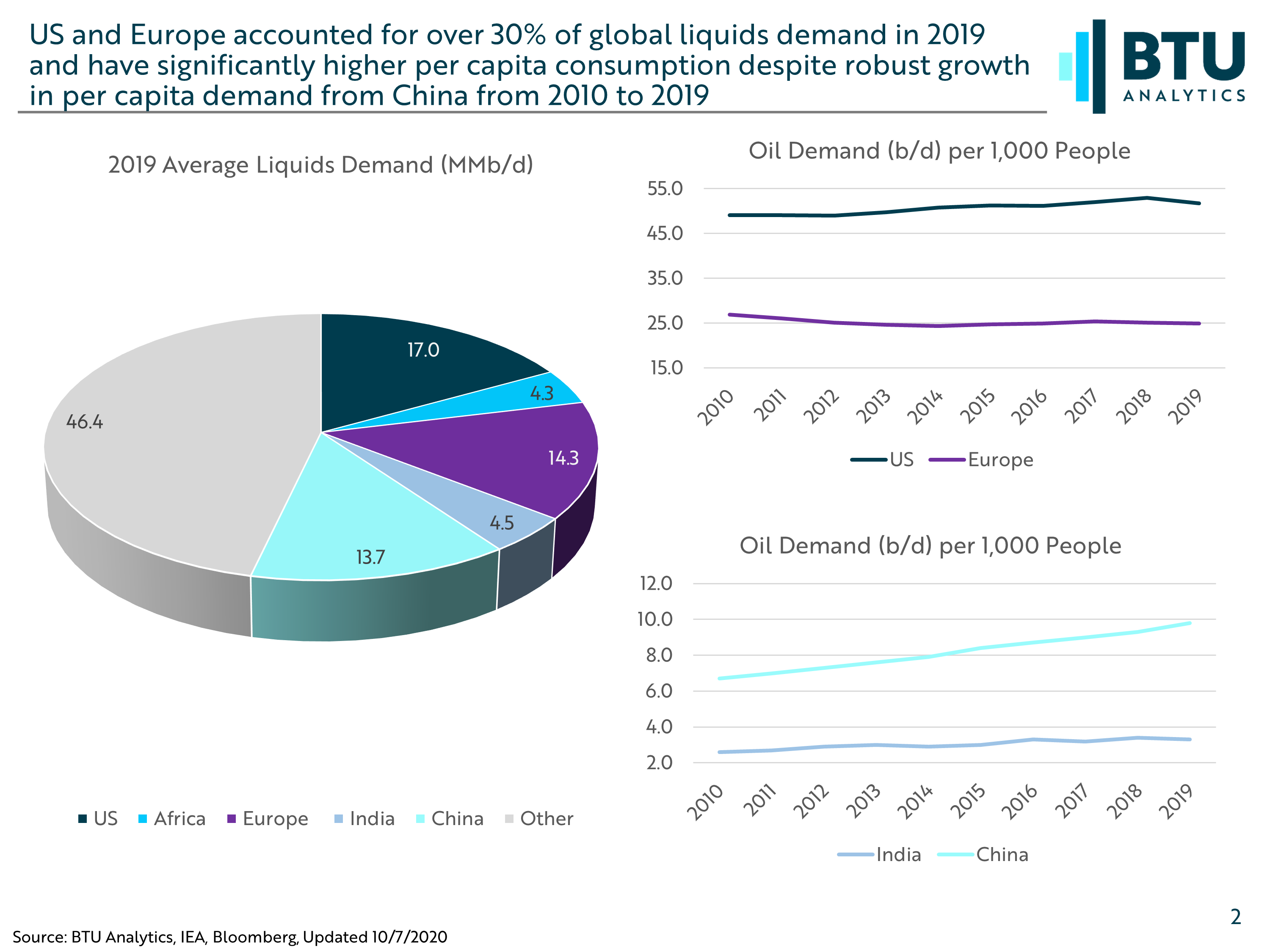

The chart below highlights Europe’s significant role in global oil demand. Europe is second only to the US in terms of total demand in 2019 and on a per capita basis.

The high oil demand per capita and the fact the restrictions were eased considerably this summer highlights just how tenuous and demand recovery is. New restrictions jeopardize the rapid recovery to 92% of the 4Q 2019 level achieved in 3Q 2020. A drop in European demand alone to 85% represents a loss of 1 MMb/d and a drop to 80% of 4Q 2019 represents 1.7 MMb/d. Under BTU Analytics’ current 4Q 2020 outlook, the global oil market is expected to be 4 MMb/d short supply as demand grows 2.5 Mb/d. This shortage will result in inventory drawdowns critical to rebalancing the market in mid-2021. However, if instead of continuing to recover and increase, demand in a region like Europe contracts, the already arduous road to recovery will be longer and continue to weigh on oil prices. For more detail on BTU Analytics’ oil price forecasts and oil market analysis request a sample of our Oil Market Outlook Report.