The last several months were marked by unprecedented destruction of demand for liquids globally, which sent forecasts from early 2020 into a tailspin. Most forecasts currently agree that the negative impacts to demand from COVID-19 have the deepest trough in the second quarter of 2019, but the variance in magnitude has larger implications relating to the speed at which global inventories will be drawn down and the path to full demand recovery. Aggressively modeling global liquids demand recovery by the end of 2020 could drive crude prices high enough to alter today’s supply outlook. Today’s commentary will examine the forecasts published in May 2020 from IEA, EIA, and OPEC in relation to BTU Analytics’ current outlook and what they imply about longer-term liquids demand outlooks.

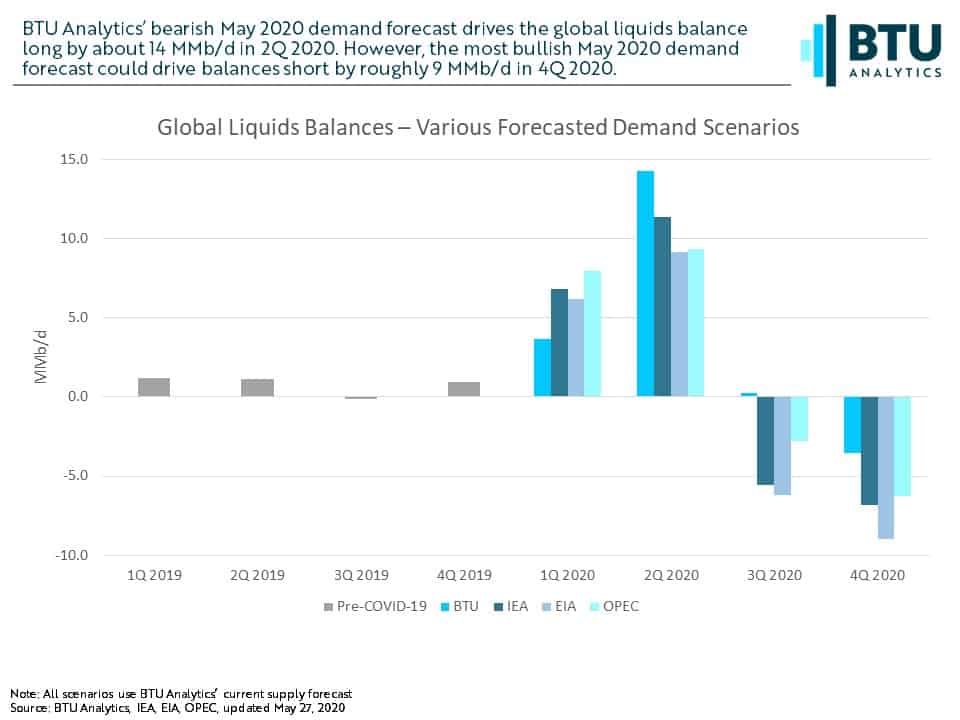

Global liquids demand deviated from its upward course entering 2020 in 1Q 2020, falling from about 100.7 MMb/d in 4Q 2019, an all-time high. This shift was driven by the discovery of COVID-19’s rapid dispersion and plummeting fuel demand as travel on all scales began to decline. This loss of demand grew in severity in 2Q 2020 as governments at several levels took restrictive measures to slow the novel coronavirus’ rate of transmission. IEA’s May 2020 forecast called for a 3.2 MMb/d increase in 2Q 2020 demand over their April 2020 forecast, citing “[b]etter than expected mobility in OECD countries with the gradual easing of lockdown measures” as the driver. The EIA and OPEC forecasts revised their 2Q 2020 demand estimates down from their prior forecasts in May based on concerns regarding travel and overall economic activity, taking the opposite revision stance as IEA. BTU Analytics’ May forecast is the most bearish of the group at 76.4 MMb/d in 2Q 2020. With new economic information surfacing daily, the true impact of the coronavirus on demand for petroleum liquids is still up for debate in the first half of 2020. However, the depth of the global demand trough in 2Q 2020 is crucial for determining the trajectory for the rest of the year.

While demand is arguably the more volatile component of balances today, what dictates prices is truly the global liquids balance, not outright demand. All demand forecasts are long in the first half of 2020 when weighed against BTU’s current supply forecast, a result of global liquids demand plummeting much faster than supply could be reigned in. The severity of liquids surplus in 2Q 2020 varies between 9.2 MMb/d from EIA and 14.3 MMb/d in our forecast. What the outlook for demand in the second half 2020 holds, quarterly balance shortfalls of up to 9.0 MMb/d based on the EIA demand outlook, could drastically impact how quickly prices will recover and potentially challenge compliance with supply cut agreements. If prices begin to rise by reacting to supply shortfalls, compliance with OPEC+ production curtailments could deteriorate, flooding the market with crude and eradicating current upward price momentum.

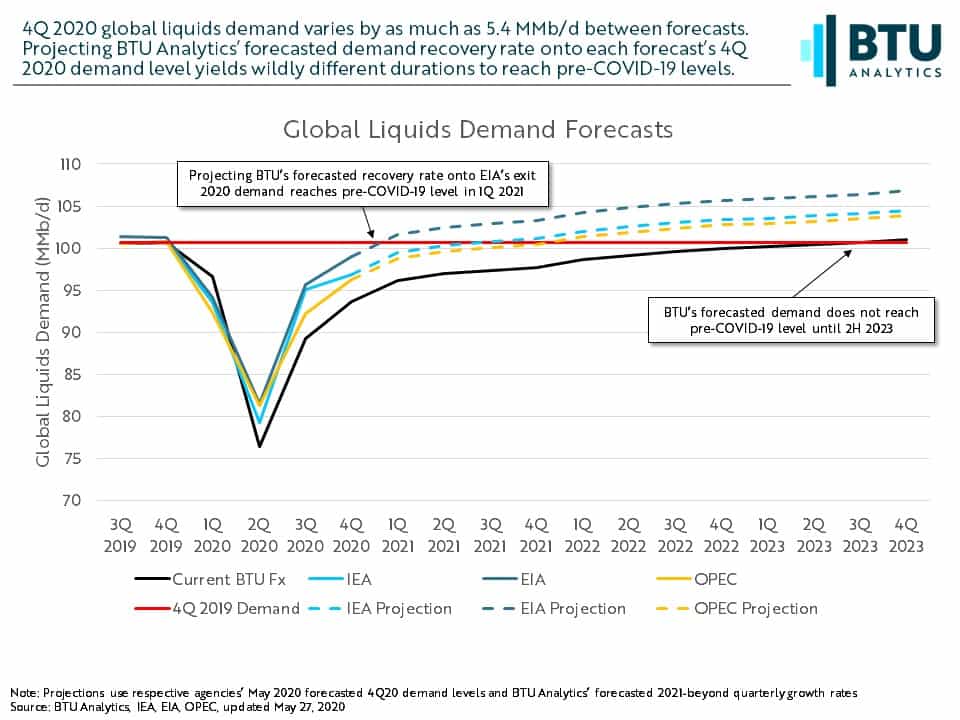

The level each forecast models demand as we exit 2020 speaks volumes about the degree of optimism baked into the assumptions. Projecting BTU Analytics’ forecasted rate of demand recovery onto the exit-2020 demand levels for all forecasts yields drastically different durations for demand to recover to the pre-COVID-19 level between forecasting agencies. BTU does not expect demand to fully recover to the pre-COVID-19 level until 2H 2023, predicated on global economic activity taking a slow recovery path. Level-shifting BTU’s projected recovery rate onto EIA’s 4Q20 demand achieves this by 1Q 2021, marking a rapid “V-shaped” recovery. Where global demand exits 2020 will be critical to determining the duration of market disruptions caused by COVID-19.

Forecasting global liquids demand in a rapidly evolving news cycle is a difficult endeavor, so recognizing the implications of short-term forecasts is crucial to determine the duration of COVID-19 market disruptions. For more information about BTU Analytics’ global liquids demand outlook, request information about our Oil Market Outlook.