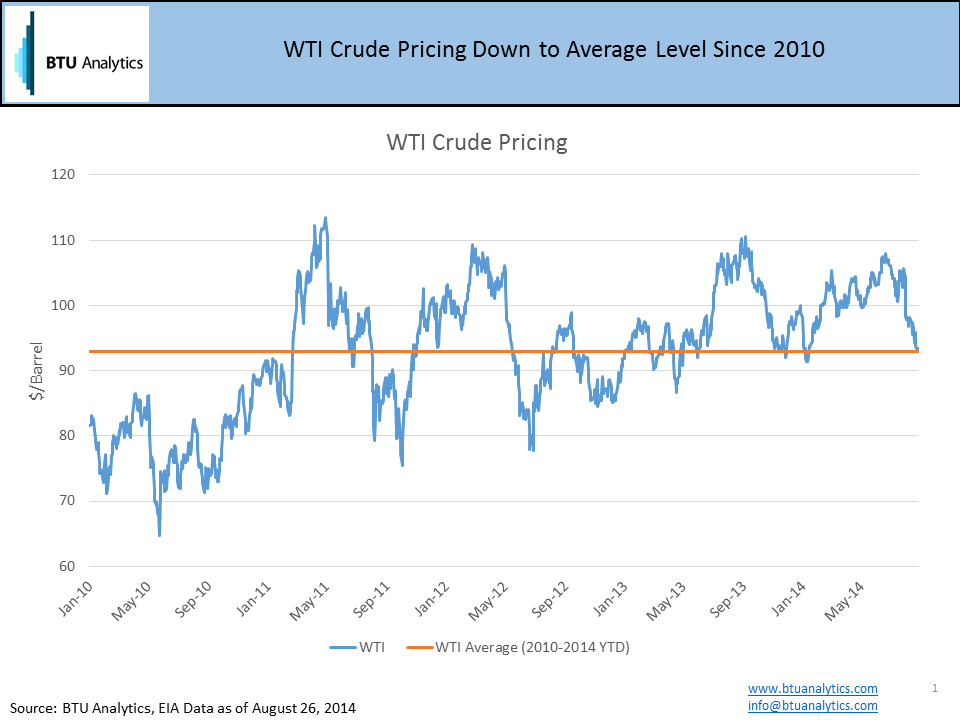

US weekly production of crude oil recently reached all-time highs of 8.57 MMb/d, meanwhile over the last month WTI has broken below the $100 per bbl mark. The recent pricing weakness at WTI has tested lows set in November 2013 and January 2014, both near $93 per bbl.

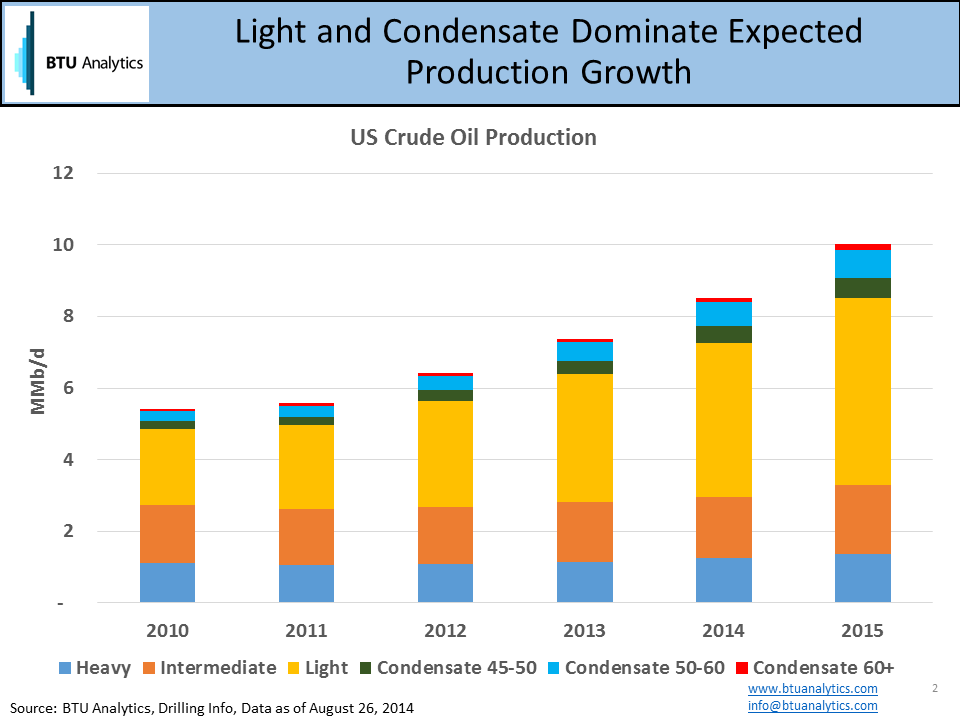

WTI breaking $100 may have psychological affects on the market, but is unlikely to deter producer investment in North America. Recent industry announcements at industry conferences show just how bullish producers are on North American plays including Powder River Basin, Wolfcamp, Bakken, Niobrara, Tuscaloosa Marine Shale, Eaglebine, and Gallup, and the returns at $100 crude. However, not all U.S. crudes are treated equally by refiners and meaningful pricing discounts are driven by transportation and crude quality. U.S. crude production growth has been driven by both light crude and condensate production. BTU Analytics estimates that light crude oil and condensate production totaled 4.5 MMb/d in 2013, will average 5.5 MMb/d in 2014 and increase to 6.7 MMb/d in 2015.

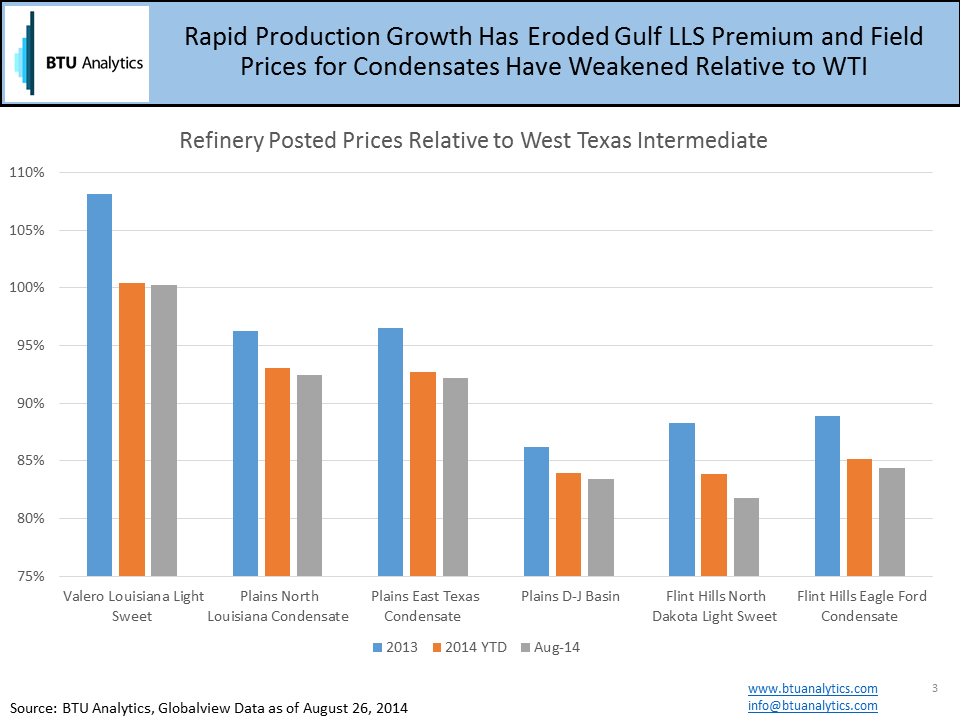

The rapid rise in production has stressed the US crude oil pipeline, refining, and rail network over the last 5 years prompting investment in over 200 crude by rail terminals and over 5 MMb/d in new pipeline capacity connecting production areas with the Cushing and Gulf Coast markets. Despite the significant investment in infrastructure, differentials for the lightest crude or condensates have been under pressure in 2014. The allowance of condensate exports by Pioneer and Enterprise was only a blip on the radar compared to overall production growth to-date in 2014. The chart below shows pricing for various North American refinery bulletin board prices as percentage of WTI. Louisiana Light Sweet (LLS) has seen its premium to WTI erode from 108% in 2013 to near parity for 2014 as increased deliveries of crude via rail and the Ho-Ho pipeline have connected the Louisiana market to additional US supply. Condensate prices in the Eaglebine and Cotton Valley plays in East Texas and Northern Louisiana have also been under pressure as producers have exhausted pipeline transportation to the Gulf Coast and have needed rail and trucking to support production. TexStar recently announced a 120-mile pipeline with a capacity of 200 Mb/d to ease constraints in the region. The weakest pricing in the Gulf Coast though has been those areas with the lightest production (Flint Hills Eagle Ford) and those furthest from market (Flint Hills North Dakota Sweet). Producers have seen discounts to WTI widen over the last several months with differentials pushing over $15 a barrel in each area.

If WTI weakens further and differentials continue to widen, how much longer can US crude oil producers sustain 1,500+ oil rigs in the field? Will new plays like the Gallup, Eaglebine, and TMS survive a lower pricing environment? Or will the US government step in and open the release valve in time for US producers to export excess crude oil to the broader oil market before the crash?