With full service on Enbridge’s Westcoast pipeline finally restored after the October 2018 outage, and continuing improvements to TC Energy’s NOVA System expected through the second quarter of 2021, natural gas takeaway capacity in the Western Canadian Basin finally appears to be turning a corner. But as gas pipelines are debottlenecked and transmission systems are improved, are Canadian producers ready to ramp up natural gas production to fill expanding capacities?

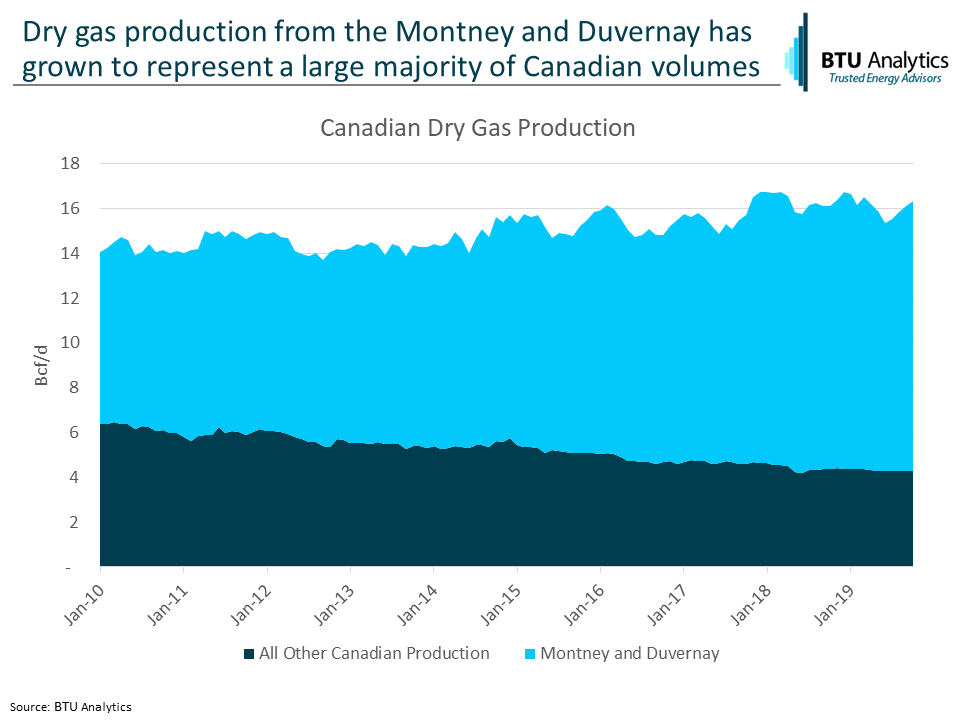

Dry gas production in Western Canada has grown incrementally over the past decade, however, sustaining and growing production has increasingly fallen to operators in the Montney and Duvernay. The portion of Canadian gas sourced from these formations has risen by almost 40% since 2010, and now represents a full three-quarters of total Canadian annual gas production. Operators in the Montney, which spans eastern British Columbia to western Alberta, stand to benefit from higher AECO prices. However, recent drilling activity in the formation suggests that producers are reducing activity, not ramping up.

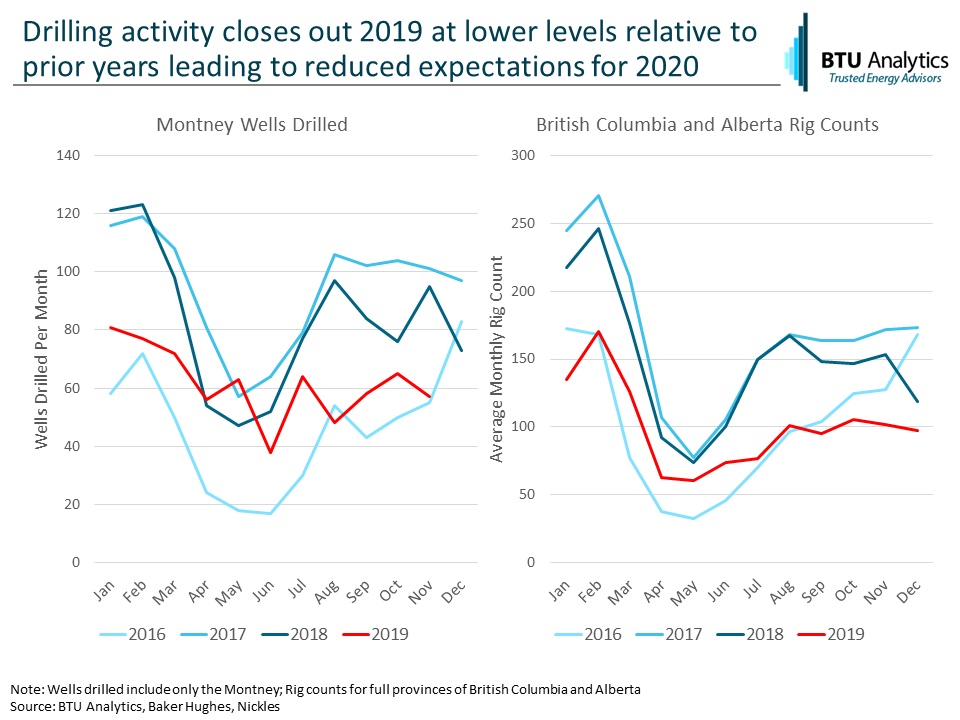

Drilling remains a highly seasonal affair in Canada, and activity in Montney is no exception. Activity typically peaks in late summer, holds steady through the fall and winter, then falls off sharply when accumulated snow and frost melt in the spring. Spring melt makes the ground soft and muddy which leads to road closures and difficulties in moving heavy drilling equipment. The number of wells drilled during mud season in 2019 was comparable to 2017-2018 averages, but activity in the latter half of the year hasn’t seen a typical recovery, instead closely retracing 2016 lows. Reduced rig counts in 2019 suggest the number of wells drilled going into 2020 will remain suppressed relative to recent years.

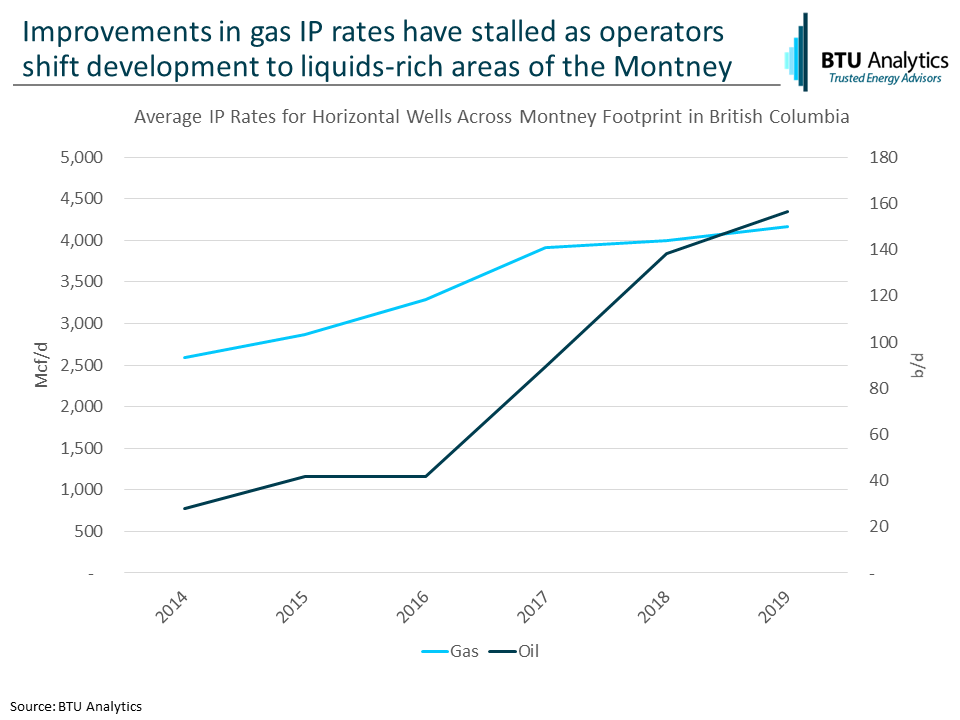

Increases in average horizontal initial production (IP) rates have helped offset declines in drilling activity in previous years, however, improvements in gas rates have stalled while oil (typically condensate) rates continue to improve. Before leveling off in 2018-2019, average gas IP rates within the Montney footprint in British Columbia surged 50% from 2014 to 2017, from 2.6 MMcf/d to 3.9 MMcf/d. Average oil rates continued to increase after gas rates stabilized, increasing from 30 b/d in 2014 to 150 b/d in 2019. As operators pivot to more liquids-rich areas in the Montney, the market may no longer be able to rely on continuous increases in gas IP rates to sustain production during periods of declining activity.

With increases in gas IP rates seemingly stalled and drilling activity falling below prior year levels, the ability of Montney producers to quickly ramp production to fill newly increased gas takeaway capacity becomes increasingly tenuous. To stay up to date on BTU’s analysis of activity and production for the Montney, Duvernay, and other US and Canadian plays, request a sample of our Upstream Outlook. For the latest outlook on pricing and flow dynamics in Western Canada, request a sample of BTU Analytics’ Gas Basis Outlook, which includes our AECO forecast as well as forecasts for other price points across North America.